A Brief History of Dollar Hatred

The current wave of animosity towards the USD is not the first - and it will not be the last.

Over the past 20 years, I have experienced 3 big waves of Dollar Hatred. I will discuss them below.

And in the appendix, I will present some hard data pertaining to the current debate about de-dollarization.

Animosity towards the dollar is elevated in 2023. But this is not in itself new, and the dollar is trading strongly, with price dynamics seemingly divorced from the media-narrative about de-dollarization. At least for now.

But first let us look at history…

Wave 1: Fear of the current account

Back in 2004-2008, I was head of currency strategy for Goldman Sachs. The dollar was dropping fast, and for multiple years. For example, the Euro rose from a low around 0.80 in 2002 to a high around 1.60 in summer 2008.

It was a time when the dollar was so hatred that some even refused to take payment in US dollars. The Brazilian top model famously announced that she would only take payment in Euro, I as re-called in my 2013 book: The Fall of the Euro.

There were multiple reasons for the dollar depreciation.

First, economies outside the US were growing strongly, in a period of arguably unprecedented globalization and optimism about emerging economies.

My boss at the time, Jim O’Neill, invented the concept the BRICs (capturing the economies with the biggest potential at the time: Brazil, Russia, India and China), and emerging market investing was very much in fashion, while US investments were perceived as more ‘boring.’

Second, there were structural issues in the US economy that concerned many, including big institutional investors around the world, and people on main street.

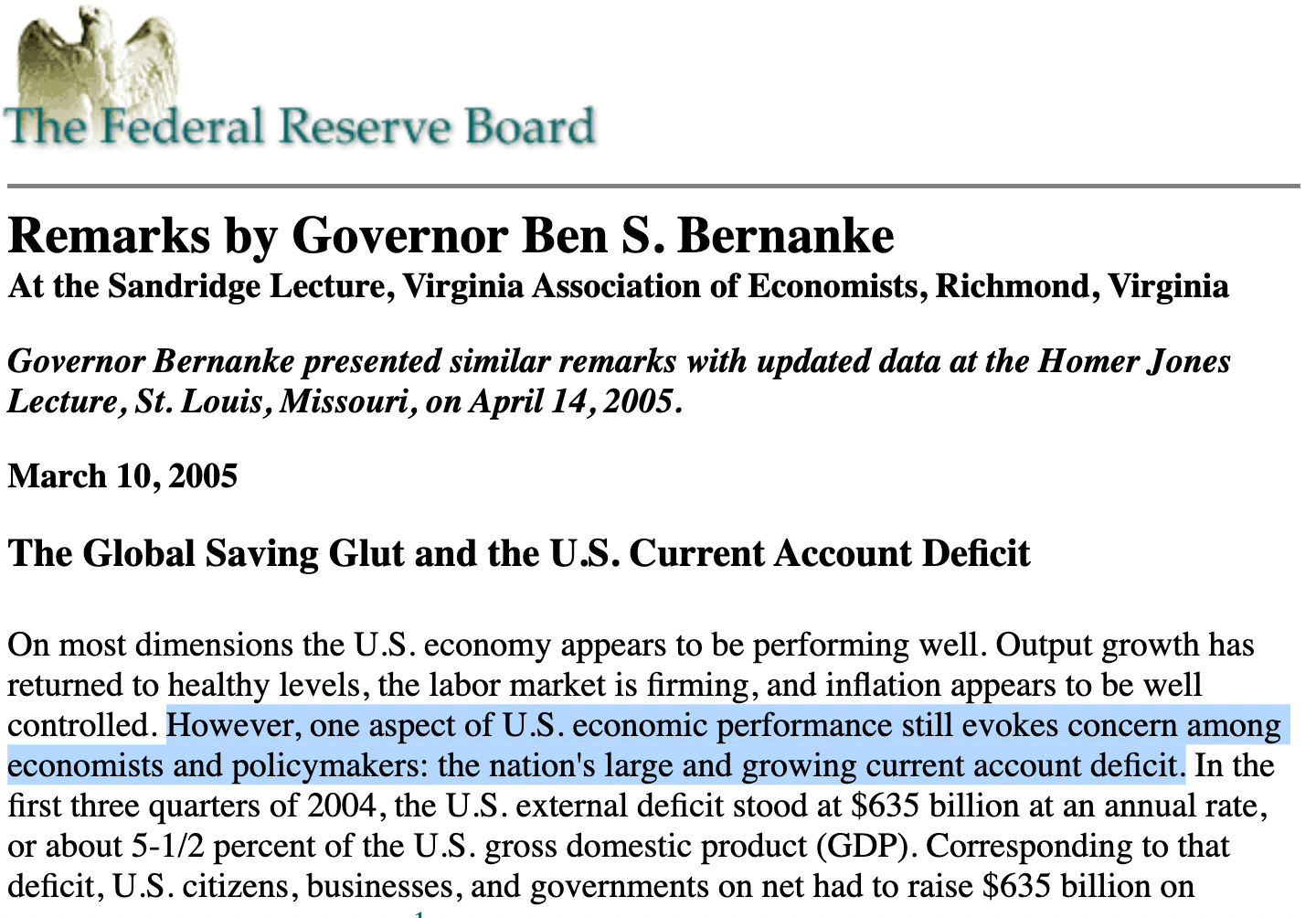

The current account got a lot of focus. And many prominent academics such as Blanchard, Feldstein, Obstfeld, Rogoff, Bernanke and Eichengreen analyzed the role of the US current account deficit, and predicted various degreed of Dollar depreciation as a result.

Since Bernanke was not only an academic, but also a prominent policy maker in that period, I have pasted a quote from his 2005 speech below.

I also recall doing a conference call with Goldman clients at the time.

No less than 1500 institutions dialled in from around the world (I was told a record at the time for a “macro call”). The topic was the extreme correlation (near 100pct) between the oil and the dollar. Week after week, especially in early 2008, the dollar declined in lockstep with rising prices for energy, so that the EURUSD chart and the Oil price chart were even hard to distinguish.

The link between oil prices and the dollar was perceived to be through the US current account (although petro-dollar recycling into Euro assets likely played a role in the background too). At the time, the US was a very big global energy importer, and the widening of the current account deficit was primarily linked to every larger costs of commodity imports (as illustrated with the expanding blue bars below).

But just as the concern reached extremes, the world changes.

The global financial crisis, triggered by tension in the US mortgage market, put in motion a series of market reversals including both the dollar (up!) and oil prices (down).

What was perhaps especially surprising to many was that the dollar strengthened, despite the cause of the crisis being mostly home-grown. An emerging market currency with a credit crisis would certainly not appreciate. But the dollar was different. The dollar shortage, which the break-down in credit markets ignited, created forced dollar buying by many borrowers around the world, supporting the USD in the process (in a way that even violated textbook equations, such as covered interest rate parity).

It is how a reserve currency behaves, and the dollar still had that special ‘magic,’ supporting it in times of crisis—even if the crisis started in the US itself.

From mid-2008, to March 2009, the dollar rallied hard against almost all major crosses, and concerns about the dollar were pushed in the background, at least for a little while.

Wave 2: QE infinity and USD de-basement concern

In the 2009-2013 period a different type of dollar hatred started to take hold.

The US trade deficit had shrunk, shale had been found (meaning that the US had to import less oil and gas), and the US was pursuing conservative fiscal policy (rightly or wrongly), which also helped reduce the current account deficit

But while concern about the trade deficit was reduced, concern about reckless monetary expansion was growing. An example below from Anders Aslund at the Peterson Institute for International Economics (link to article from 2010, here)

The concern about monetary expansion is understandable in the context of the experimental nature of the policy as the Fed expanded their balance sheet aggressively to combat deflationary forces.

The dollar did trade down notably as EM (and Europe) bounced back strongly from the GFC partly based on historical stimulus in China (from which China is still suffering.)

There was even talk about a currency war, as some EM currencies such as the Brazilian Real ‘suffered from’ historical fx strength.

But this period also ended.

It was a combination of the euro crisis which ended a trend of EUR strength, China’s bop crisis in 2015, which ended years of asymmetric inflows into CNY, and the Fed’s ability to start a hiking cycle on its own in 2014.

What followed was a multi-year period of dollar gains

Initially due to global weakness (which triggered QE and negative rates around the world), then due to Covid (and demand for US risk assets) and finally due to aggressive Fed rate increases and elevated fixed income vol.

Wave 3: China, USD weaponization & de-dollarization

This current period of dollar hatred has been about potential de-dollarization by EM countries, linked to China’s efforts to create an alternative reserve currency and CNY-based payments system, as well as potential fall out from ‘too aggressive’ sanctions on Russia around the Ukraine invasion in 2022 (including de facto confiscation of Russia’s reserves in G7 countries).

But there are holes in this narrative.

In the appendix I repeat arguments I made at the Fed’s dollar conference in May (see also my twitter thread here).

Bottom line: THERE IS NO OBVIOUS ALTERNATIVE TO THE DOLLAR CURRENTLY.

Of course, not everything is well in the US. There is the debt ceiling and obvious political challenges—which leads to concerned texts such as I received last week.

Further, US policy makers are likely looking with concern at the growing list of anti-US alliances: BRICS, China-Russia, Saudi-Russia, Brazil-China, Indonesia-Iran etc etc.

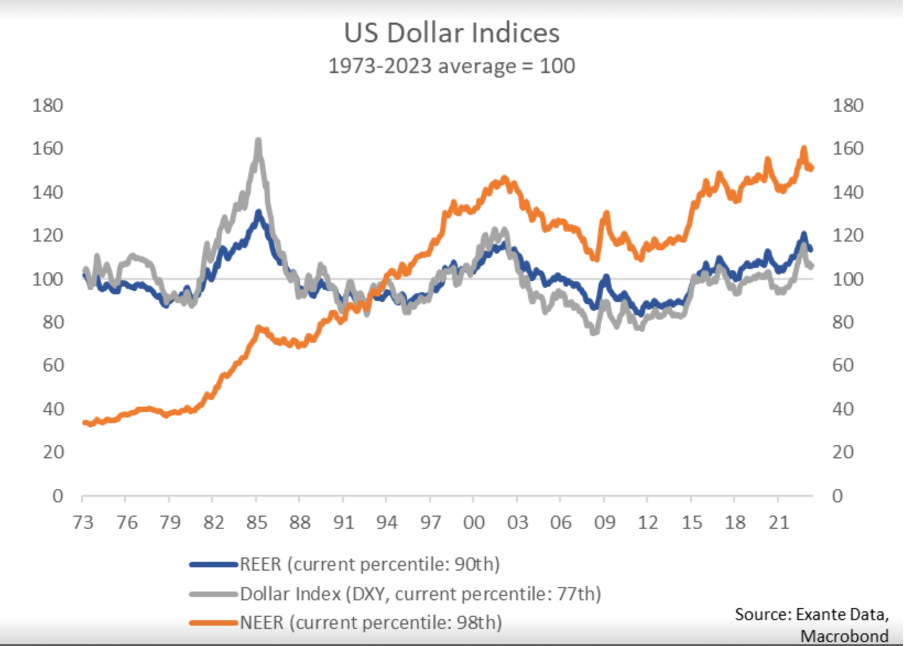

But it is always worth looking at what the market is saying. There is no long-term trend of USD decline. It always depends on which dollar index you look at. But regardless of the index, you will find that the USD is above its long-term average, in nominal and real terms currency, despite all the Dollar Hatred.

Another way to look at the same data is to see where the USD is trading vs history in specific crosses (not index level). More color on this chart in this short video.

The dollar is not weak. The dollar is strong. Perhaps not in the narrative told. But in the actual market is is.

At Exante Data we form currency views based on holistic global data analysis (within conceptual frameworks we have developed over multiple decades). There are many moving parts in the USD outlook, and at various points, we have advised institutional clients to trade the USD both long and short 2023. We do not believe that one single variable (such as the de-dollarization ‘variable’) dominates all other variables, and we will continue to adopt a pragmatic multi-variable approach to USD strategy.

APPENDIX: Background Information on USD Capital Flows Adapted from twitter tread with slides from my NY Fed Presentation

Two weeks ago, I spoke at the NY Fed's “Dollar Conference.” Below, we summarize five observations from the conference, which tries to qualify the debate about de-dollarization with capital flow analysis.

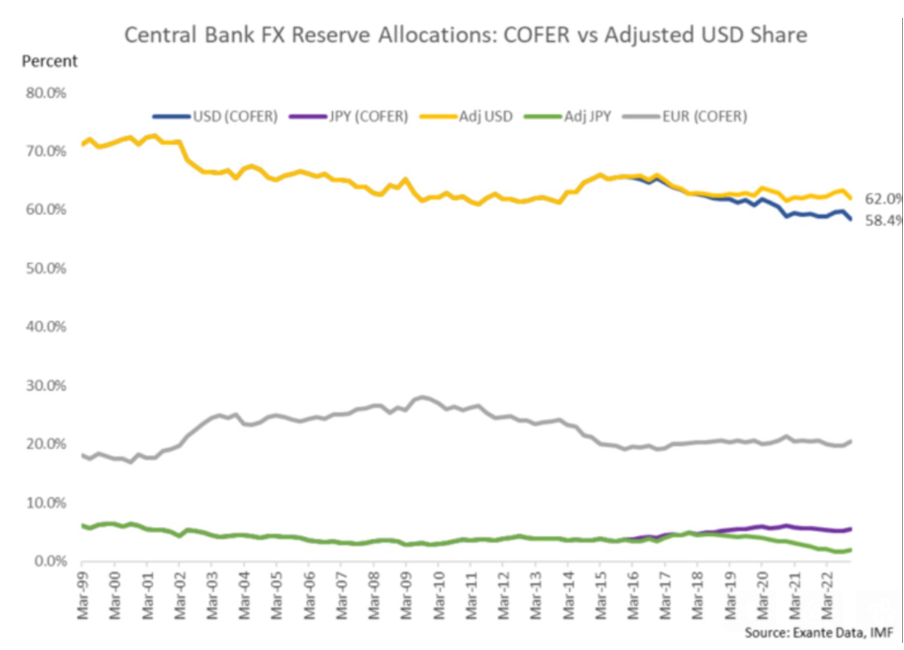

First, there is a lot of focus on the declining USD share of global reserves. But the COFER data does not include derivatives, and this will mean that USD is understated.

Above, we have estimated the degree to which the JPY share may be overstated (when you take into account JGBs exposure swapped into USD), and this then bumps up the USD share. We do not have good global data on this. But the RBA has stated that this effect can be big.

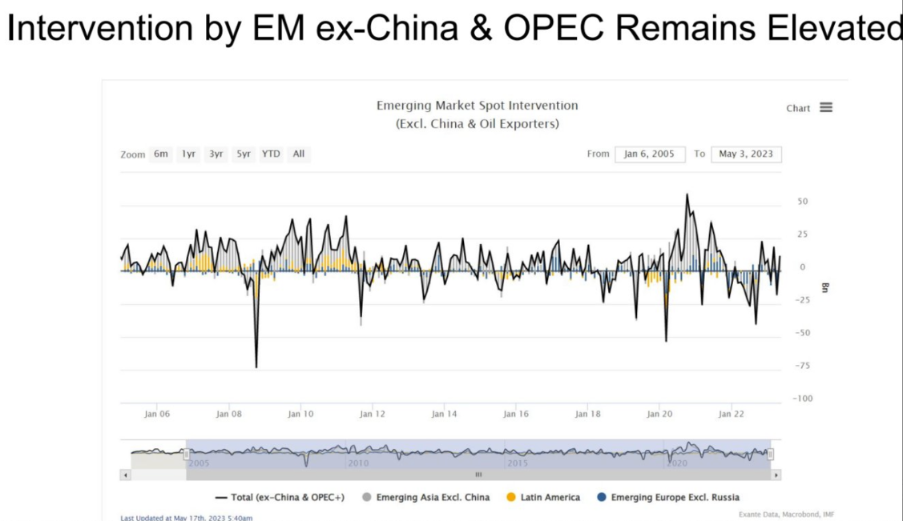

Second, Global currency intervention (some would call it 'currency manipulation') has declined somewhat since the period period and after the GFC. But that is mostly because China is trying to intervene less.

Outside of China and OPEC, intervention trends are in line with history (EM sample.)

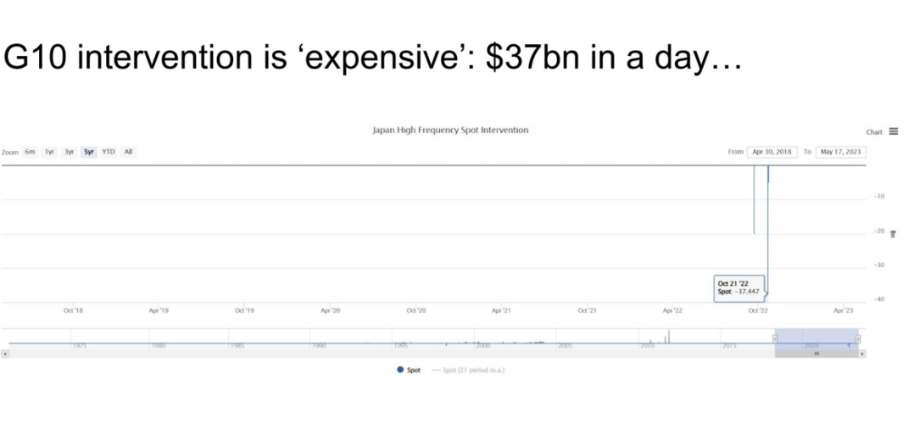

And outside of EM, we have more activity again, with Japan selling FX for the first time in decades, in 2022, and Switzerland has been very active.

Bonus chart: It is expensive to intervene in G10 markets...

Third, there is some evidence that high reserves can help keep a currency stable (Think Taiwan Dollar = TWD, not Turkish Lira = TRY.)

But it gets more complex when you include G10 countries (look at the Norwegian Krona: super-high reserves, and still a lot of volatility.)

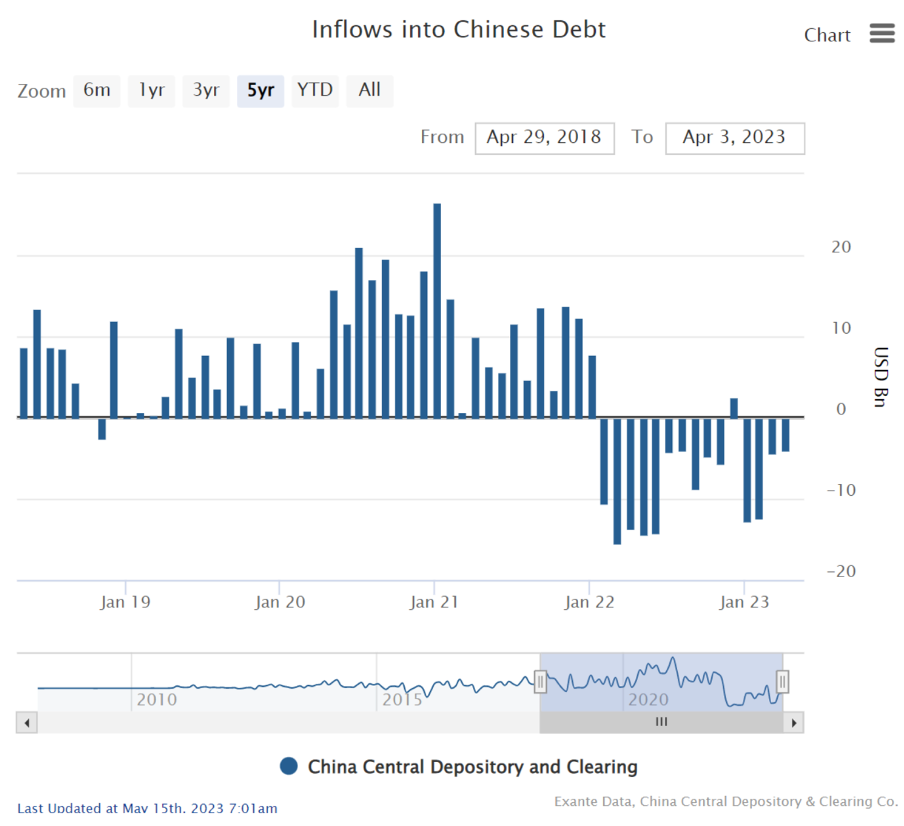

Fourth, as part of the de-dollarization debate, there is focus on increasing flow into gold. But the official reserves data, submitted to the IMF (which we collect) is less bullish than the World Gold Council data. It would be great if the WGC could elaborate more...

Fifth, the dollar is facing challenges: High deficits, political tension (just look at the debt ceiling debate), reduced role in international trade, more global political opposition (from China, BRICS, etc). But what is the alternative? Nobody wants Chinese bonds...

Even central banks, using COFER data from the IMF, have been scaling back on their CNY exposure in recent quarters, in a set-back to the more constructive trend in previous years. The CNY is not regarded as an attractive alternative to the USD, at least not yet.

The dollar's exorbitant privilege remains, even if: 1/ domestic US forces are increasingly unhelpful, and even if 2/ the US's role in global trade is on decline. And the simple explanation is that it is so hard to find an alternative attractive reserve asset.

The content in this piece is partly based on proprietary analysis that Exante Data does for institutional clients as part of its full macro strategy and flow analytics services. The content offered here differs significantly from Exante Data’s full service and is less technical as it aims to provide a more medium-term policy relevant perspective. The opinions and analytics expressed in this piece are those of the author alone and may not be those of Exante Data Inc. or Exante Advisors LLC. The content of this piece and the opinions expressed herein are independent of any work Exante Data Inc. or Exante Advisors LLC does and communicates to its clients.

Exante Advisors, LLC & Exante Data, Inc. Disclaimer

Exante Data delivers proprietary data and innovative analytics to investors globally. The vision of exante data is to improve markets strategy via new technologies. We provide reasoned answers to the most difficult markets questions, before the consensus.

This communication is provided for your informational purposes only. In making any investment decision, you must rely on your own examination of the securities and the terms of the offering. The contents of this communication does not constitute legal, tax, investment or other advice, or a recommendation to purchase or sell any particular security. Exante Advisors, LLC, Exante Data, Inc. and their affiliates (together, "Exante") do not warrant that information provided herein is correct, accurate, timely, error-free, or otherwise reliable. EXANTE HEREBY DISCLAIMS ANY WARRANTIES, EXPRESS OR IMPLIED.

Another reason that CNY cannot unseat USD as the major reserve currency is that it would require China to have an open capital account, which is not going to happen anytime soon.

Interesting article... Will include it in my Monday Emerging Markets Link post...