A New Driver of China's De-Dollarization

The $100bn surge in Chinese trade credit since 2024 has been denominated in renminbi - that's new and opens up a new avenue for China and the rest of the world to de-dollarize.

Chinese banks have begun to provide substantial amounts of renminbi-denominated trade financing in the last 1-2 years. The current scale is not unusual per se. What is notable is that the financing now seems to be heavily renminbi-denominated.

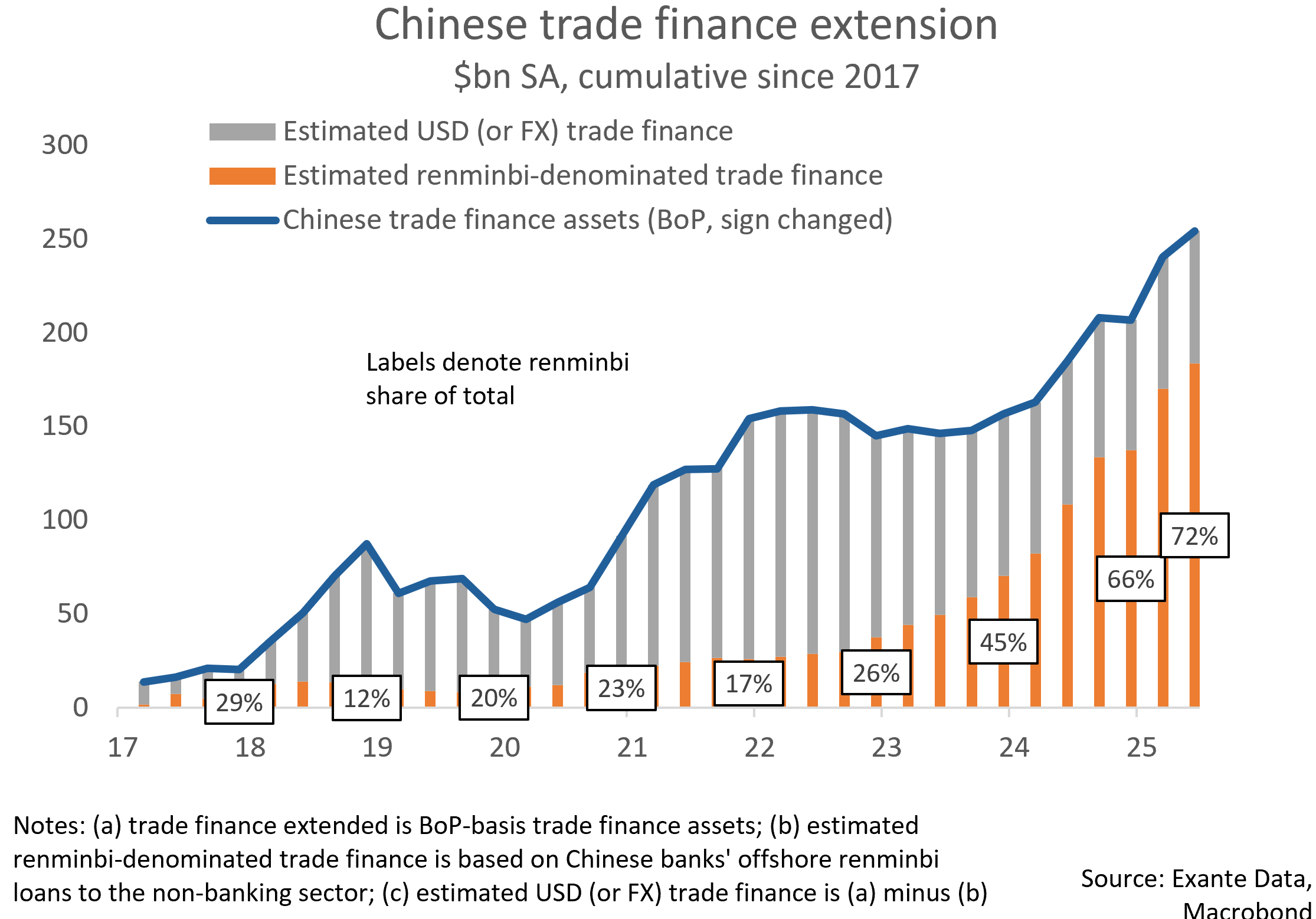

Chinese trade credit added up to around $150bn during 2017-2021, and only 17% was in RMB. However, since 2022, the composition has changed, and renminbi has grown so quickly that it now makes up 72% of the cumulative $250bn extended since 2017. In other words, the Dollar share of Chinese trade credit is dropping sharply. In fact, the provision of USD trade credit may be negative.

This note is based on excerpts from a report sent to clients of Exante Data.

Introduction

Last year, the share of global trade financing denominated in renminbi began to correlate closely with Chinese BoP-basis trade finance credits. What’s more, Chinese trade credit flows have corresponded nearly one-for-one with Chinese banks’ external renminbi loans since 2024. Authorities in both Hong Kong and mainland China have also provided support for CNH trade financing, though announced policies might not have been the biggest driver of the expansion (behind-the-scenes support from mainland authorities might have mattered more). Russia moving away from USD usage has likely also played a role, particularly in 2022, though Russia alone is too small to account for the whole phenomenon.

Taken together, we conclude that a substantial portion (perhaps nearly all since 2024) of new Chinese trade credit loans appears to be denominated in CNH, though a large share of the stock of trade credit probably still remains denominated in dollars.

The rise of renminbi-denominated trade financing also fits well into the broader political goals. Renminbi-denominated financing should make Chinese exports more resilient to geopolitical tensions by making sure foreign consumers can buy Chinese goods even if they lose access to the global dollar system. In addition, if Chinese exporters get paid in renminbi (as a result of the RMB-denominated trade credit), they will presumably be more likely to reinvest their earnings into their local operations or purchase Chinese assets - and won’t have any dollars to “recycle”. That would support the domestic economy, the renminbi, and reduce holdings of US assets over time.

At Exante Data, we are hyper-focused on how the shifts in the global economic order are impacting FX markets. We have previously looked at this in the context of changing allocations to the dollar (link) at large and for China’s shifting dollar allocations in particular (link). In this note, we show how trade finance - which gets little attention - has also become a major driver of Chinese de-dollarization recently.

Chinese trade finance: $100bn increase in trade credit provision in 1.5 years; RMB-denominated financing dominates, which is new

Trade credits “arise from the direct extension, during the normal course of trading, of credit from a supplier to a buyer—that is, when payment for goods and services is made at a time that differs from the time when ownership of the underlying goods or services change” (IMF definition).

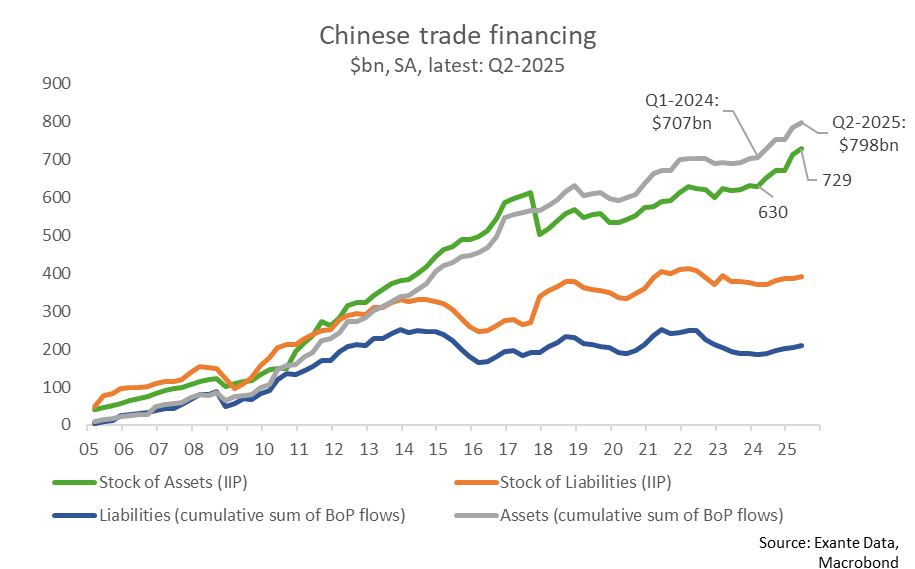

In China’s case, trade credit assets, whereby Chinese resident companies provide trade finance credit to non-resident buyers of Chinese goods, are larger and growing more quickly than trade finance debits. After remaining stable during 2022-2023, the stock of trade credit assets (financing to buyers of Chinese goods) increased from $630 billion in Q1 2024 to $729 billion in Q2 2025 (see chart below). In contrast, trade credit liabilities have remained flat.

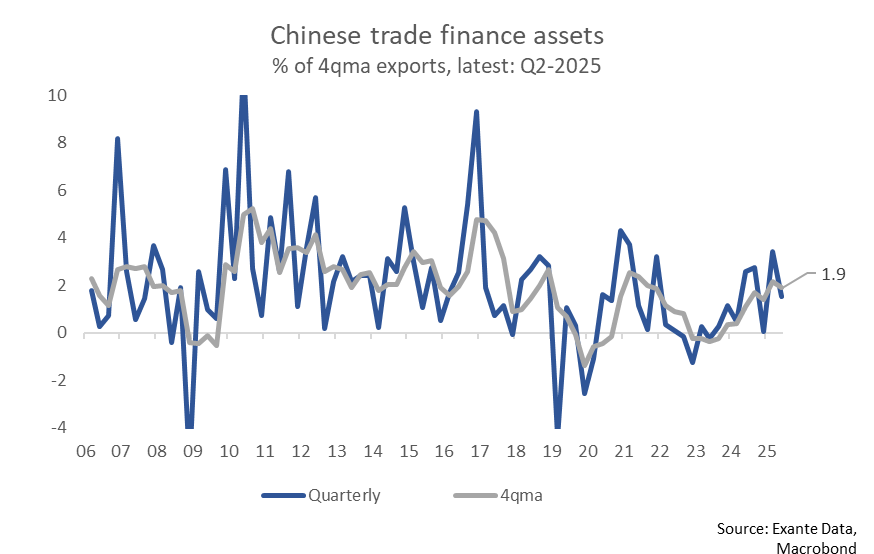

As a share of exports, trade credit extension has risen from around 0% in 2023 to around 2% in Q2-2025, in line with the long-term (2006-2025) average of 2.0%. The denominator (exports) has risen a lot over time, of course, and means that the dollar amount of trade credit provision is large now.

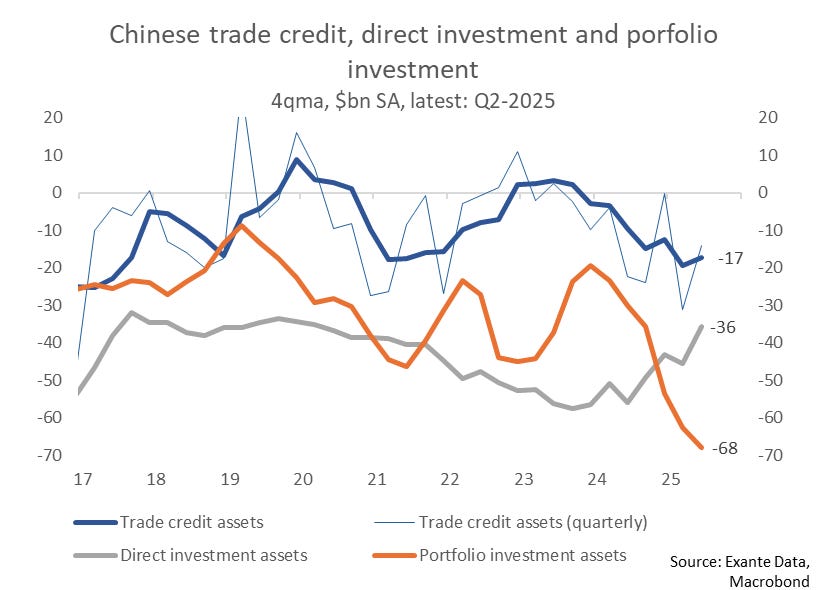

Another way to contextualize trade credit is by comparing it to other BoP categories. Trade credit assets stood at $17bn in Q2-2025 on a 4qma basis, around half the size of outbound (direct investment assets) or a quarter of portfolio investment outflows (assets).

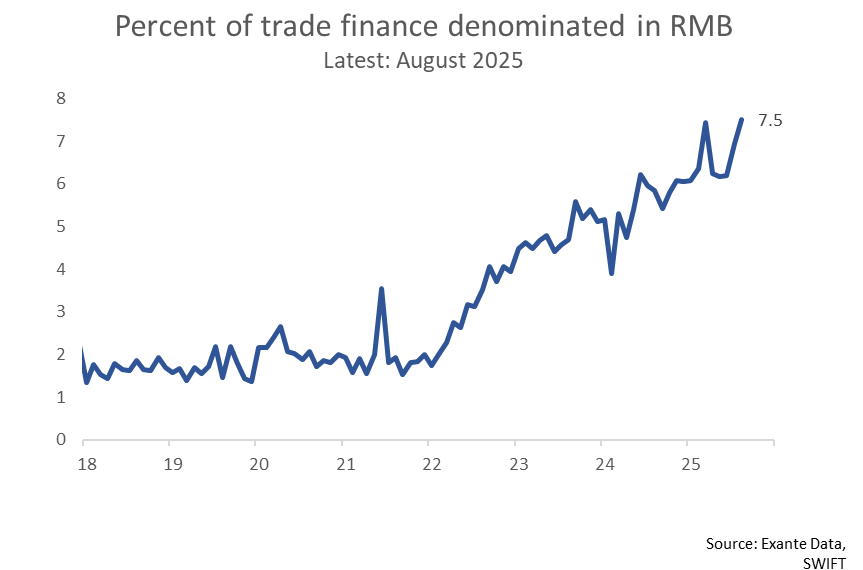

Though trade credit provision only began to grow substantially in 2024, the share of global trade credit denominated in renminbi started increasing following Russia’s invasion of Ukraine in 2022 and hit a record of 7.5% in August 2025, according to SWIFT. The rise in trade credit provision in 2022 might therefore have involved converting dollar-denominated (Russian) trade credit into renminbi-denominated trade credit without increasing the overall size of financing. This is indeed what a recent study from the Fed finds: “The currency denomination of cross-border lending by Chinese banks globally shifted suddenly away from dollars to RMB starting in 2022”.

The total size of Russian trade in 2021 (gross imports + gross exports) was around 1.8% of global trade, whereas Russia-China trade was around 0.3% of total global trade. The share of global trade credit denominated in RMB increased by 2.7%-pts between January 2022 and January 2023. Trade isn’t the same as trade credit, of course, though these numbers suggest that Russia might have driven a substantial portion of the “renminbi-ization” of trade credit during 2022. However, Russia is too small to account for the 5.5%-pts increase in the RMB share since 2021 (2.0% average in 2021 to 7.5% by August 2025). It’s worth keeping in mind here that overall (CNH) trade credit did not begin to increase notably until 2024. The conclusion is that the story goes beyond what “Russia effects” alone can explain.

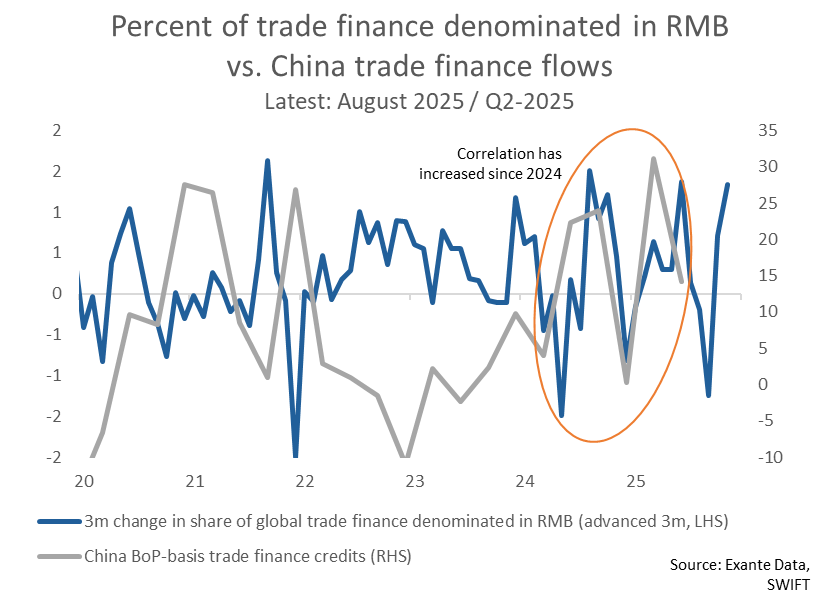

The correlation between RMB-denominated global trade financing and Chinese trade finance provision used to be very weak, as we can see in the chart below, suggesting that trade financing probably tended to be denominated in dollars.

But since 2024, Chinese trade credit flows have begun to correlate with changes in the share of global trade financing that is denominated in renminbi. This is the first sign that Chinese firms are increasingly providing trade financing denominated in renminbi rather than dollars.

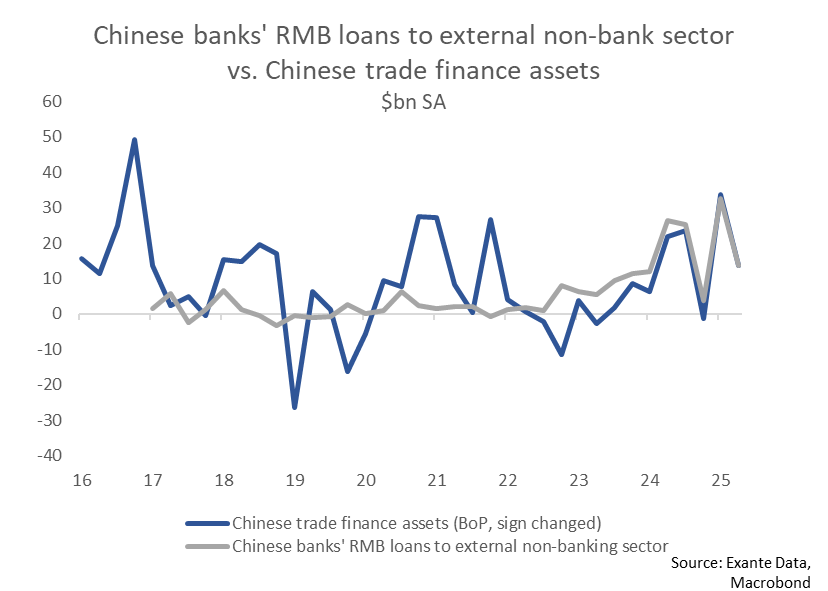

Another piece of evidence is that there has been a close linkage between trade finance provision and Chinese banks’ RMB loans to the external non-banking sector since last year (see chart below). This makes us rather convinced that the increase in trade financing has been mainly (or arguably almost entirely) denominated in renminbi. It is noteworthy that the correlation between these two series used to be rather weak until 2023, which yet again supports the idea that RMB-denominated trade financing is a new phenomenon.

The content in this piece is partly based on proprietary analysis that Exante Data does for institutional clients as part of its full macro strategy and flow analytics services. The content offered here differs significantly from Exante Data’s full service and is less technical as it aims to provide a more medium-term policy relevant perspective. The opinions and analytics expressed in this piece are those of the author alone and may not be those of Exante Data Inc. or Exante Advisors LLC. The content of this piece and the opinions expressed herein are independent of any work Exante Data Inc. or Exante Advisors LLC does and communicates to its clients.

Exante Advisors, LLC & Exante Data, Inc. Disclaimer

Exante Data delivers proprietary data and innovative analytics to investors globally. The vision of exante data is to improve markets strategy via new technologies. We provide reasoned answers to the most difficult markets questions, before the consensus.

This communication is provided for your informational purposes only. In making any investment decision, you must rely on your own examination of the securities and the terms of the offering. The contents of this communication does not constitute legal, tax, investment or other advice, or a recommendation to purchase or sell any particular security. Exante Advisors, LLC, Exante Data, Inc. and their affiliates (together, “Exante”) do not warrant that information provided herein is correct, accurate, timely, error-free, or otherwise reliable. EXANTE HEREBY DISCLAIMS ANY WARRANTIES, EXPRESS OR IMPLIED.