Argentina's new EFF

What's in the new program?

In April, just before the Spring Meetings and to much subsequent fanfare, the IMF and Argentina unveiled a new program—a 48-month Extended Fund Facility (EFF) arrangement of USD20bn with an immediate disbursement of USD12 billion to build gross reserves.

We wrote about the floating band and reserve accumulation since (here and here.)

Last week, the Petersen Institute for International Economics (PIIE) had a seminar where we learned about the concern of participants that Argentina’s adjustment is resulting in an overvalued real exchange rate—stabilisations that pivot on such overvalued often end in tears. But we didn’t learn much about the new program itself.

Was the fanfare about the EFF warranted? Here are five features of the April program that are worth noting.

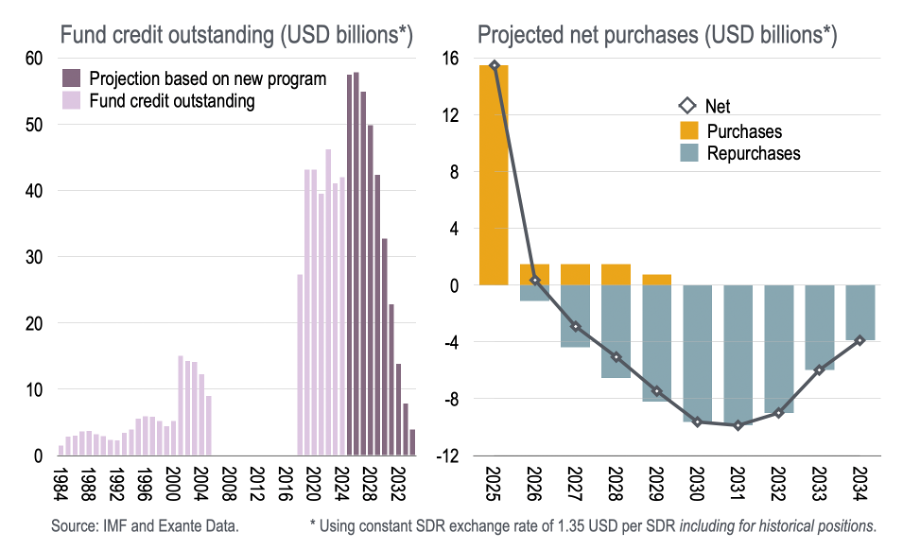

1. Program financing

If it disperses as planned, the new EFF program will take total credit outstanding to the Fund to USD57.8bn at the end of 2026, the highest in history. Net purchases this year of USD15.5bn is set to be followed by USD0.3bn in 2026 after which net repurchases from the Fund of USD2.9bn in 2027, USD5.1bn in 2028, increasing to a peak of USD9.9bn in 2031.

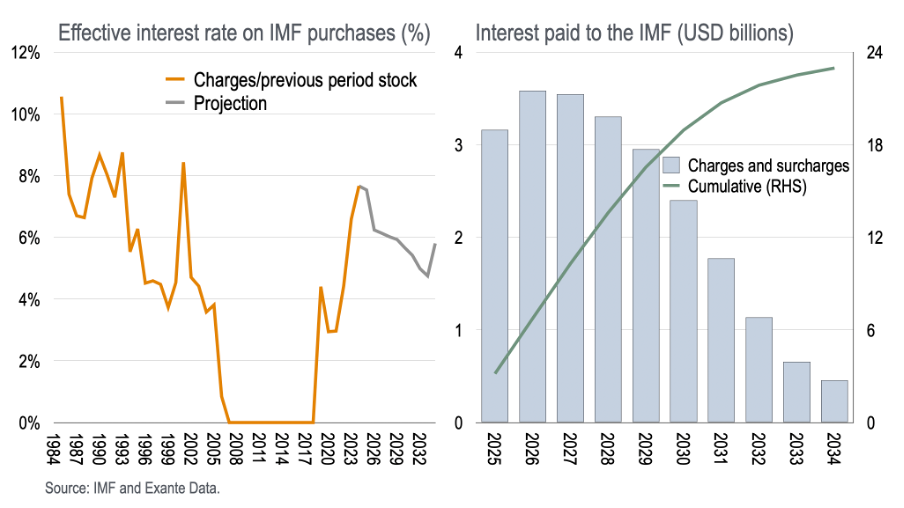

The net interest paid on the program borrowing over the next decade sums to nearly USD24bn—at the SDR rates as they were in April. This is on top of interest and charges since 2018, of course.

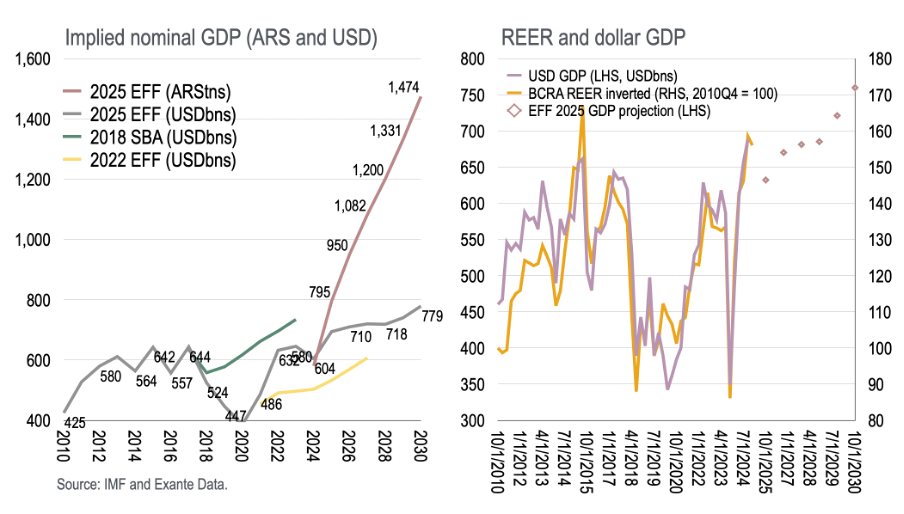

2. GDP

The assumed path for nominal GDP in dollars rings alarm bells, redolent of past Fund forecasting failures.

The program assumes dollar GDP increases to USD780bn in 2030.

Since dollar GDP historically maps fairly closely into the level of the real exchange rate—here as measured by the BCRA index since 2010, inverted—this is equivalent to assuming the real exchange rate experiences a real appreciation to a record high over the next 6 years. The possibility of such real appreciation alongside current account surpluses (see below) seems odd.

The 2018 Stand-By Arrangement (SBA) could be, and was, reasonably criticised for the heady dollar GDP projections that resulted in optimistic debt-to-GDP forecasts. The EFF appears to have resorted to the errors from 2018 once more.

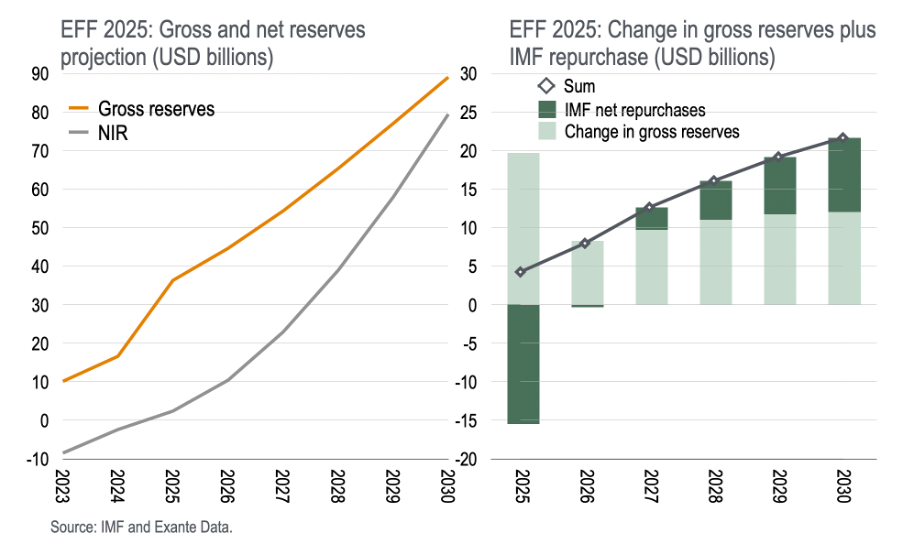

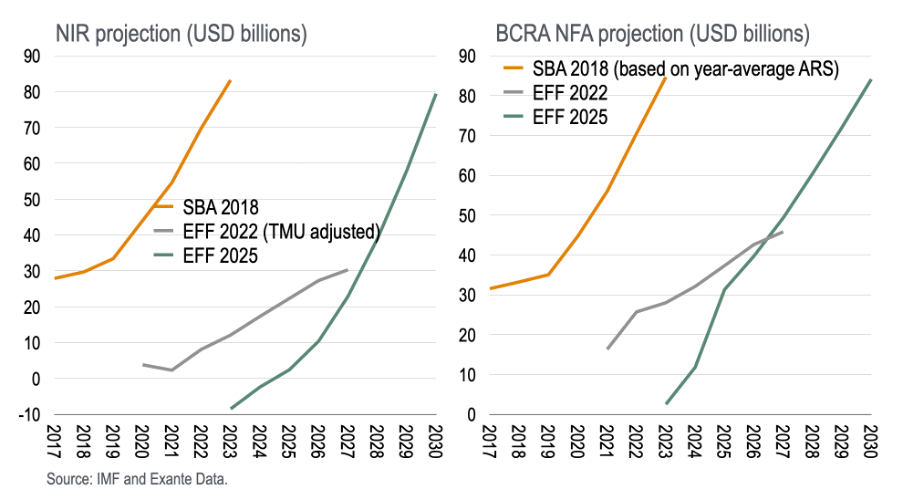

3. Capital flows and reserves

The burden of interest payments and repurchases over the program horizon is not expected to hinder Argentina’s capacity to accumulate international reserves under the program, however.

Gross reserves are projected to increase to nearly USD90bn by 2030 while net international reserves (NIR) are protected to reach USD80bn.

Net IMF repurchases plus reserve accumulation cumulate to USD82bn over the next 6 years (2025 inclusive.) If we add to this the interest projected on IMF lending over this period, more than USD100bn in “below the line” flows are expected through 2030—which, of course, require an “above the line” counterpart in autonomous private sector activity.

To put this in the context of recent programs, the NIR and NFA accumulation under the new EFF is even more ambitious than the 2018 SBA noted above in the context of growth optimism (detail on assumed capital flows can be read here).

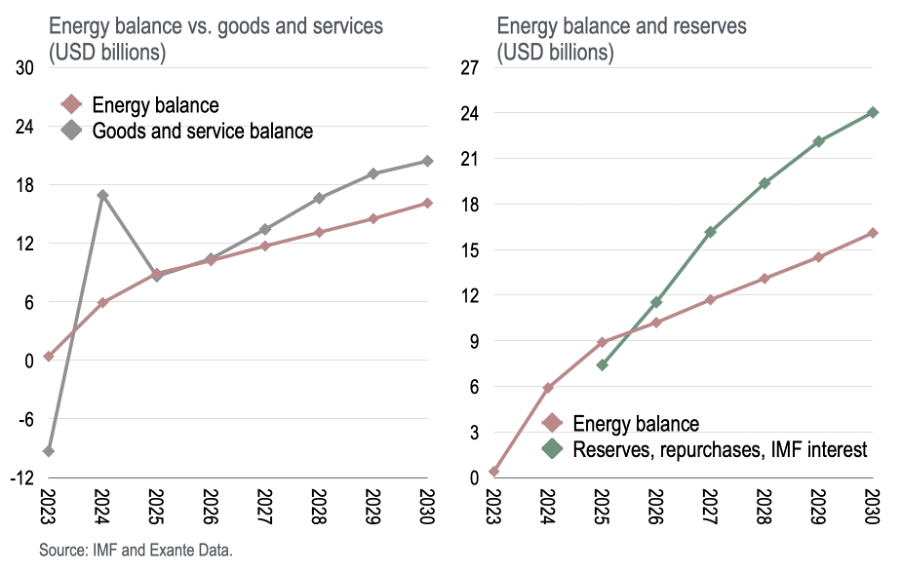

4. Energy balance

An important difference in the EFF compared to previous programs is the assumed increase in net energy exports, even if the assumptions are somewhat more conservative than those suggested by BCRA.

This is reasonable in the sense that deregulation under the Milei government and improved property rights has unleashed enthusiasm from investors in the energy sector (see here.)

As such, net energy exports are projected to increase from USD0bn in 2023 to USD16bn in 2030. This supports the goods and service surplus which is expected to reach a record high in 2030. But this alone is not enough to facilitate reserve accumulation plus IMF repurchases and interest—the “below the line” flows noted above.

Yet if Argentina can indeed “save” all the projected energy balance surplus over the next 6 years, this will facilitate three-quarters of cumulative official foreign exchange needs over the forecast—including IMF repurchases.

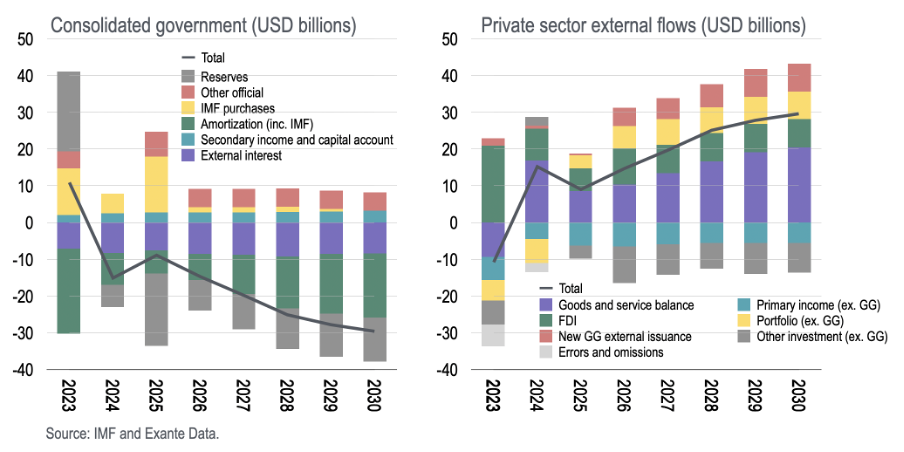

Put another way, decomposing the balance of payments private “autonomous” flows, we see that the goods and service surplus plus net FDI inflows roughly track the consolidated government “below the line” net external financing flows—or balance of payments in the traditional sense.

Other private sector flows (net portfolio inflows versus primary income debit plus other investment outflows) roughly balance.

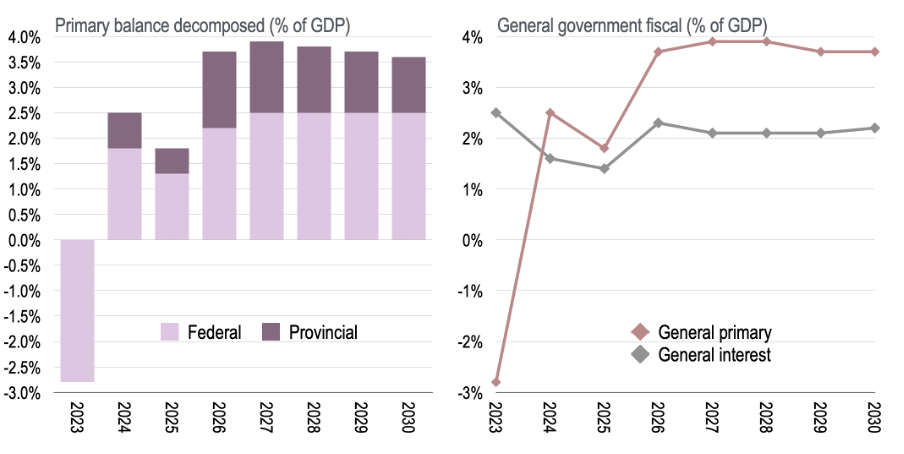

5. Fiscal and monetary

Another important difference at this time, compared to past programs, is the up front fiscal adjustment due to President Milei. The primary balance moved from near-3% deficit in 2023 to near 2.5% surplus including the provinces in 2024. The primary surplus is expected to drop about 0.7ppts in 2025 (an election year) before further adjustment in 2026 and 2027.

It is noteworthy that the provinces are expected to generate about one-third of the primary surpluses—while the general government interest bill remains subdued at only about 2% of GDP. Whether either of these are realistic is questionable.

In any case, it is also noteworthy that the fiscal deficit is not recorded properly. Interest payments on “zero-coupon bonds issued prior to 2025” are included “below the line” (see Table 3b on page 49, for example.) As such, the deficit is under-reported and it is not clear what the true fiscal stance is.

Moreover, the links between the government and central bank have not been completely cleared up.

Under the EFF, BCRA gets transferred USD11bn of reserves while government repays some non-marketable claims. And part of the cost of conducting monetary policy has been transferred to the government. But beyond that, it is not clear that central bank balance sheet clean-up has been completed or that a further recap will not be necessary.

One only needs to look at the projected increase in BCRA balance sheet during a period of expected huge reserve accumulation, and wonder how this is being sterilised. Let’s just say it doesn’t make sense!

Summary

In some senses, the new EFF is back to the 2018 IMF approach under Macri—the program hinges on hope rather than design. In summary:

Nominal GDP projections look optimistic, thus making debt projections unrealistic;

Balance of payments projections and reserve accumulation look unlikely given the implied real exchange rate appreciation;

Net energy exports may help, but it is not clear the private saving rate will increase as required—as banks return to business once more their lending will drive domestic demand and imports;

Central bank balance sheet weakness is not resolved as part of the program (still);

The fiscal accounts understate the deficit and fold coupons into financing.

The content in this piece is partly based on proprietary analysis that Exante Data does for institutional clients as part of its full macro strategy and flow analytics services. The content offered here differs significantly from Exante Data’s full service and is less technical as it aims to provide a more medium-term policy relevant perspective. The opinions and analytics expressed in this piece are those of the author alone and may not be those of Exante Data Inc. or Exante Advisors LLC. The content of this piece and the opinions expressed herein are independent of any work Exante Data Inc. or Exante Advisors LLC does and communicates to its clients.

Exante Advisors, LLC & Exante Data, Inc. Disclaimer

Exante Data delivers proprietary data and innovative analytics to investors globally. The vision of exante data is to improve markets strategy via new technologies. We provide reasoned answers to the most difficult markets questions, before the consensus.

This communication is provided for your informational purposes only. In making any investment decision, you must rely on your own examination of the securities and the terms of the offering. The contents of this communication does not constitute legal, tax, investment or other advice, or a recommendation to purchase or sell any particular security. Exante Advisors, LLC, Exante Data, Inc. and their affiliates (together, "Exante") do not warrant that information provided herein is correct, accurate, timely, error-free, or otherwise reliable. EXANTE HEREBY DISCLAIMS ANY WARRANTIES, EXPRESS OR IMPLIED.