Back to the nineties

Argentina and the Fund turn back the clock

There are definite similarities between the situation facing Argentina today and in the 1990s:

Both followed uncomfortably high inflation (though the late-1980s hyperinflation was worse than the more recent manifestation);

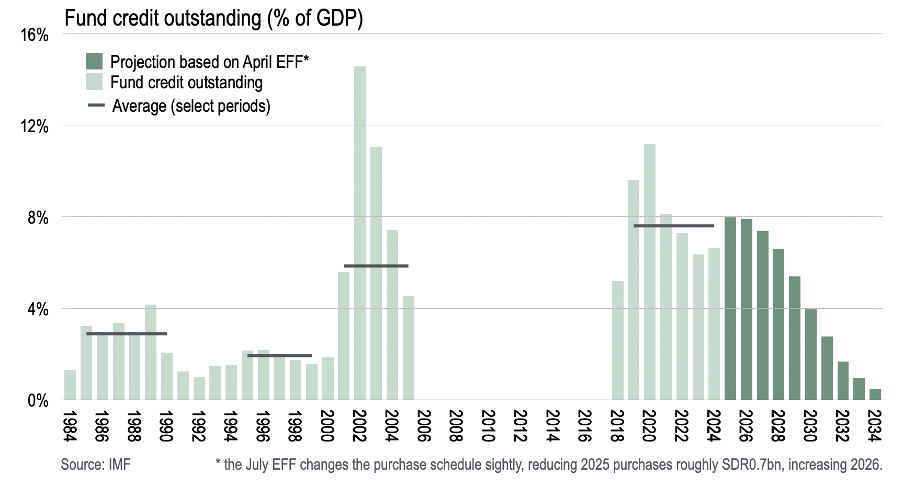

They both follow protracted—and require ongoing—IMF engagement though back-to-back SBA or EFF programs (though IMF exposure today at 8% of GDP is higher than the 2-3% in the 1980s and 1990s.)

Both attempt stabilisation on a foundation of a very low stock of gross and net international reserves (then under a currency board, today a dirty float);

Finally, both periods require tight fiscal policy (though the 1990s turned out to be hiding looser-than-ideal fiscal.)

Most important, perhaps, the growth cycle in the 1990s was different: due to bank credit creation and private sector spending, something happening once more today under President Milei.

Yet the 1990s did not end well for Argentina. It might be useful to draw lessons from that decade.

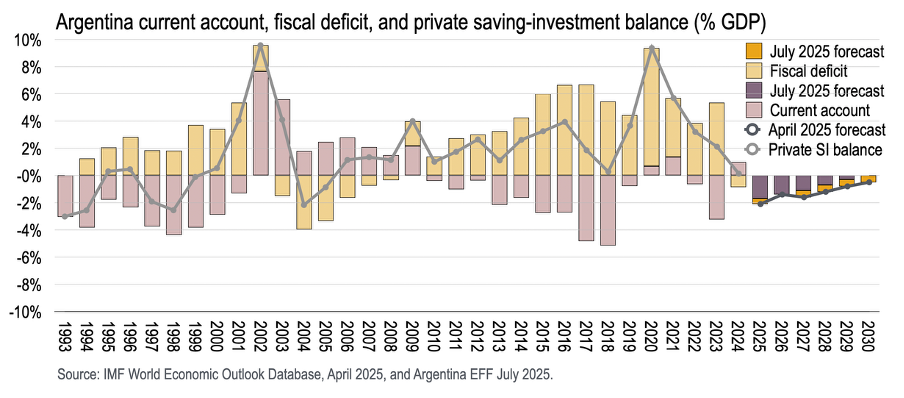

Private saving-investment

Indeed, the latest IMF program document (the EFF First Review) implies that Argentina’s private sector saving-investment balance—the sum of the external current account and fiscal deficit, thus the accumulation of net financial claims by the private sector on either the domestic government or rest of the world—will print negative for the first time for 20 years in 2025 and to remain in deficit over the forecast horizon.

And Argentina is expected to register a private SI-balance alongside current account deficit for the first time since 1999—at the end of a period when private deficits drove a fluctuating and ultimately unsustainable external imbalance.

In other words, under the fiscal adjustment of President Milei, Argentina’s cycle is changing.

It ought to be a recognised, then, that the external deficit will now be a function of private spending, consumption and investment, rather than fiscal largesse—so that the growth for the foreseeable future will be led by the private sector facilitated by the banking system. But as the 1990s witnessed, a credit boom does not guarantee external sustainability nor the attainment of balance of payments targets—both of which are crucial for the success of the IMF’s ongoing program engagement.

Early signs of a credit boom

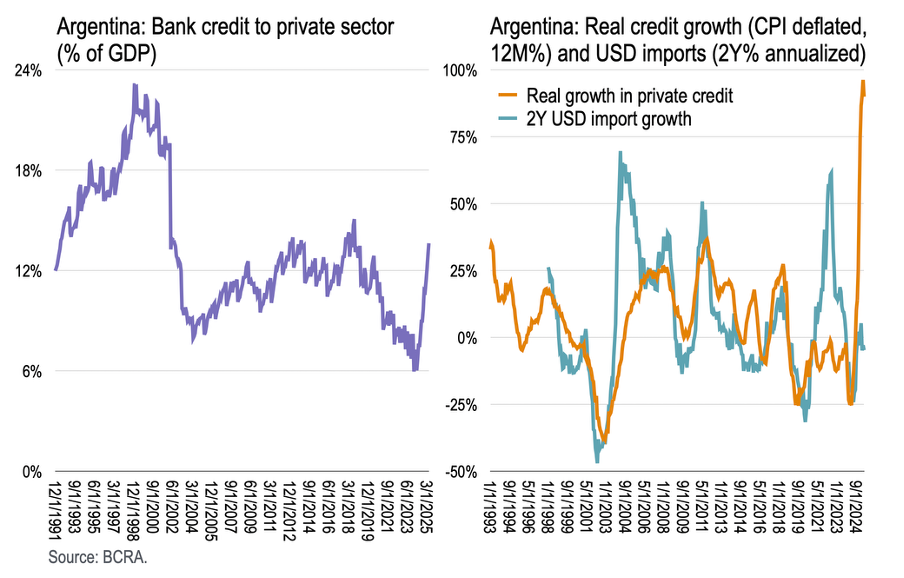

Consider bank credit to the private sector.

While the austerity of the Milei government is well-publicised, less appreciated is the credit-led boom that has now begun redolent of the 1990s.

Between end-1991 and end-1998, bank credit to Argentina’s private sector (mainly FX dominated then, not today) increased from 12% of GDP to just below 24% of GDP. This 10ppts of GDP increase came in two stages. Through 1995 there was a period of wider current accounts due to private SI-balance deficits—then a pause around the Mexico crisis. Thereafter, from 1996 to 1998, credit expanded further, when the external deficit widened to more than 4% of GDP—a threshold beyond which Argentina seldom ventures without a crisis.

Deflated by CPI, real credit growth in Argentina historically maps reasonably well into dollar import growth over 2 years (annualised). And the expansion in bank credit since late-2023 is on a scale not witnessed before—certainly not over such a short period.

This real expansion in bank credit to the private sector is close to 100% over the last 12 months—that is, real credit has doubled. More puzzling is the lack of associated dollar imports, though perhaps the banking system is simply facilitating a sustained spike in imports that began during the pandemic that would otherwise collapse during Milei’s austerity.

Despite this sharp credit impulse, private loans from the banking system remain relatively low still compared to GDP. The prospect of further credit expansion in coming years is possible if not highly likely. This would then drive further import expansion, weighing on the current account deficit.

A continually fudged program

In 1994, Jeffrey Sachs complained that the IMF was not cable of cobbling together the program needed to support Russia’s transition to a market economy: “it is a huge mistake to leave the situation up to the current IMF mission now in Moscow. The IMF lacks the vision and conceptual framework to work out any satisfactory arrangement with the Russian Government.” He suggested that the US Treasury “should take over the active guidance of the negotiations with the Russian Government from the IMF.”

Sachs in particular lamented how the analytics of monetary stabilisation was not understood by Fund staff—hence Russia could not shake off inflation during the early years of the post-communist transition.

While the situation in Argentina is very different, the Fund’s programming failings today remain.

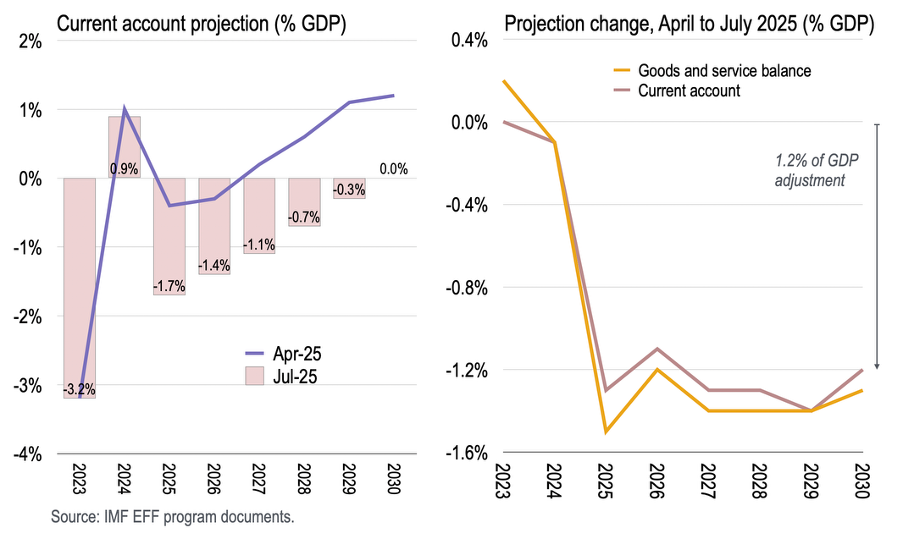

Consider some of the revisions to the latest EFF document.

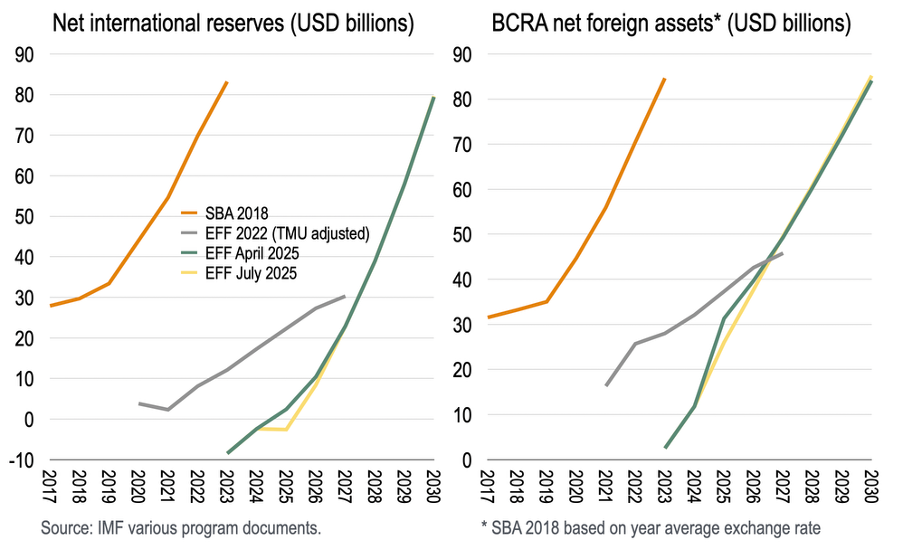

Given the wider Q1 current account courtesy of the ongoing credit boom, the July EFF revised the current account projection by 1.2% of GDP from 2025-2030. The current account now remains in deficit throughout the decade before touching exactly 0% in 2030.

This has not impacted projected net international reserves, however, which—after a digression in 2025 and 2026 due to lack-of-programmed FX accumulation of late—will return exactly to the prior expected path from 2027 to 2030—to the point where the latest projection (in yellow) is invisible in the chart below!

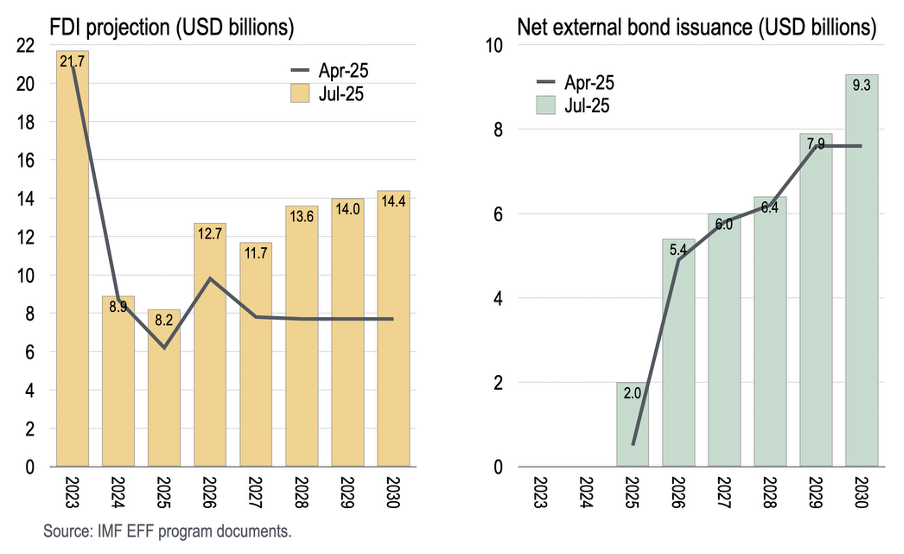

Unchanged NIR projections are possible because Fund staff remarkably discovered net FDI inflows and, to a lesser extent, net external debt issuance to fill three-quarters of the gap that would otherwise emerge—with the remaining missing part filled through more minor tweaks. How serendipitous indeed that private direct investment inflows facilitate almost exactly the current account deterioration thus leaving projected reserves unchanged.

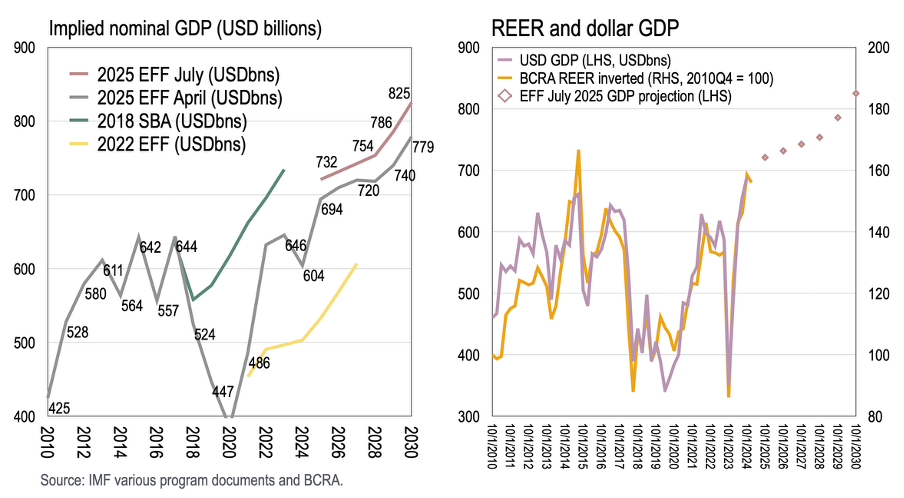

Moreover, the new EFF program has revised up an already outrageous NGDP projection so that GDP now reaches USD825bn in 2030—and correspondingly debt-to-GDP looks even more favourable than before despite overshooting prior expectations this year. Based on past relations, this suggests continued real exchange rate appreciation from today’s already stretched levels that would surely see the external current account deficit widen to well above 4% of GDP!

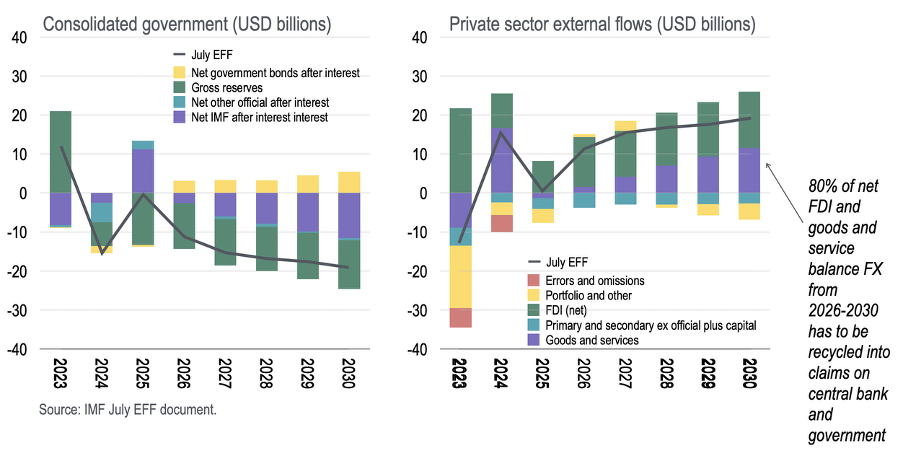

Of course, the balance of payments is not only an accounting concept, but analytically (ought to) divide external flows into those autonomous transactions due to the private sector—under the influence of domestic and global policies—and the balancing flows with the consolidated government. Such a decomposition for the Argentina program is shown in the chart below (the black lines are mirror images and sum to zero.)

The left chart illustrates how, under the program, Argentina’s consolidated government is expected to accumulate net claims on the rest of the world between 2026 and 2030 of USD80bn (shown here as negative), largely by way of gross international reserves accumulation (USD59bn) and repayment of IMF purchases and interest (USD38bn) only partly offset by net issuance to non-residents after interest (USD20bn) and sundry other official flows (USD2bn).

The right chart shows then shows the corresponding external transactions by Argentina’s private sector. Notably, net FDI inflows plus an expected goods and service surplus generate USD100bn in FX over these 5 years to facilitate net private interest payments and some foreign asset accumulation on top of the above-noted consolidated government’s net FX accumulation. As such, 80% of the net FDI inflows plus goods and service surplus from 2026 to 2030 will be required to facilitate the official sector balance of payments flows.

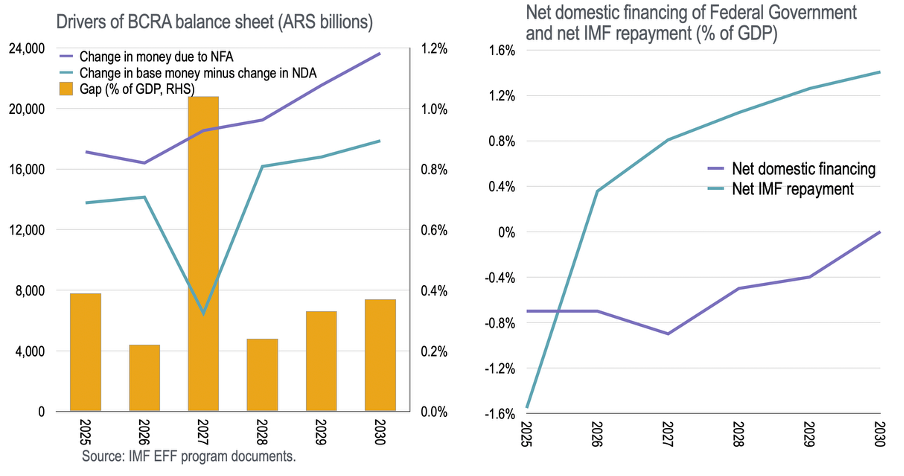

If we were to take the above balance of payments flows seriously—though arguably we should not—we might expect to see a counterpart increase in domestic private sector claims on the central bank (BCRA) and Federal Government. Yet, while navigating such thorny issues as the valuation adjustments on FX assets on the BCRA balance sheet as well as the correct accounting for “other items net” in the IMF document, we uncover no corresponding financial flows. To wit:

The implied increase in base money on the central bank balance sheet due to net foreign asset accumulation is not met by an equivalent increase in base money net of the change in net domestic assets (i.e., sterilisation or increasing government deposits with the central bank). (Note, the demise of BCRA securities has now been replaced by “credit to the financial sector, ex. securities” within BCRA net domestic assets projected as negative, implying growing deposits by the domestic non-monetary financial sector (pension funds?) which serves to sterilise some of the growing domestic liquidity required in the program. Sadly, it is not clear on what terms such deposits are remunerated and whether BCRA is therefore able to manage such sterilisation operations without later monetising the costs as during 2018-23.)

In any case, turning to the fiscal accounts, instead of there being an increase in net domestic financing of the government—that is, recycling part of the private external FX flows to facilitate IMF repurchases—the program envisages negative net domestic financing as primary fiscal surpluses are used to repay resident liabilities as well as the IMF. For a country desperately needing searching for safe domestic assets on competitive terms, not increasing issuance and building a yield curve makes no sense. This would be one sensible way to recycle any external foreign exchange, including by offering more generous interest for residents (instead of implied financial repression.)

All of this is to suggest that the IMF, to echo Jeffrey Sachs, is not up to the task. Management and staff lack the “vision or conceptual framework” to help Argentina navigate the necessary external adjustment. Given that Argentina is on the receiving end of the largest Fund program in history with substantial risks to global taxpayers, this is a pretty frightening situation.

One is tempted to suggest, given what is at stake, that the US Treasury should indeed directly take control of the negotiation to safeguard Fund resources—the task that financial programming was intended to achieve but which has been allowed to lapse.

Conclusion

This summer Britain has experienced, if not endured, a wave of Britpop nostalgia to accompany a successful Oasis reunion—putting the 1990s back in vogue.

Happily, in the Western Hemisphere, Argentina and the Fund are themselves bringing back the nineties. But unlike the feuding Gallagher brothers, it seems unlikely Argentina and the Fund will get along well enough to see the current decade through without another a major bust up.

Why? The Fund does not have a framework for balance of payments analysis—yet are engaged in the largest program in history based on flawed analysis and lapsed safeguards for international taxpayer money.

The correct course of action from here is to acknowledge past failings and construct a program that gives Argentina a decent roll of the dice—including by offering Fund resources at zero interest, as the Europeans were forced to offer Greece, to give Argentina a chance at reserve accumulation for stability and growth.

The content in this piece is partly based on proprietary analysis that Exante Data does for institutional clients as part of its full macro strategy and flow analytics services. The content offered here differs significantly from Exante Data’s full service and is less technical as it aims to provide a more medium-term policy relevant perspective. The opinions and analytics expressed in this piece are those of the author alone and may not be those of Exante Data Inc. or Exante Advisors LLC. The content of this piece and the opinions expressed herein are independent of any work Exante Data Inc. or Exante Advisors LLC does and communicates to its clients.

Exante Advisors, LLC & Exante Data, Inc. Disclaimer

Exante Data delivers proprietary data and innovative analytics to investors globally. The vision of exante data is to improve markets strategy via new technologies. We provide reasoned answers to the most difficult markets questions, before the consensus.

This communication is provided for your informational purposes only. In making any investment decision, you must rely on your own examination of the securities and the terms of the offering. The contents of this communication does not constitute legal, tax, investment or other advice, or a recommendation to purchase or sell any particular security. Exante Advisors, LLC, Exante Data, Inc. and their affiliates (together, "Exante") do not warrant that information provided herein is correct, accurate, timely, error-free, or otherwise reliable. EXANTE HEREBY DISCLAIMS ANY WARRANTIES, EXPRESS OR IMPLIED.

If your clients receive technical analysis significantly more complex than this, they must all be PhD's :)

Good take here.