BOE communication challenges

The Bank of England slips back into old habits

Amongst the highlights of the Exante Data 10th Anniversary conference in New York at the end of March was the speech by the Bank of England’s external MPC member Alan Taylor.

Taylor’s speech was an important intervention after the sell-off in UK rates the previous week, including as a result of communication during the March policy meeting. Available here, the speech was an opportunity to carefully reflect on the inflation outlook and the trade-offs involved in setting policy at this time. Taylor’s thoughts are applicable to other central banks as well and are worth a read.

Remit

To be sure, even before Taylor spoke in late March, his approach to an energy shock was well telegraphed. Speaking in early March at a conference on the Monetary Policy Mandate at the Norges Bank in Oslo, Taylor emphasised how the Bank of England’s

…mandate requires us to consider the trade-off between pushing inflation back toward target quickly versus incurring too much output volatility, following a large shock to the economy. That was the case after the inflation shocks of 2021 and 2022, and especially after the Russian invasion of Ukraine caused energy prices to spike.

In fact, it is worth re-visiting the Bank’s Remit (the latest here) to consider how this trade-off is explained there.

Indeed, the core concept of flexible inflation targeting involves the Bank communicating the associated trade-offs as a crucial part of the mandate. The Remit notes that:

The [UK monetary policy] framework is based on the recognition that the actual inflation rate will on occasion depart from its target as a result of shocks and disturbances. … Attempts to keep inflation at the inflation target in these circumstances may cause undesirable volatility in output due to the short term trade-offs involved, and the Monetary Policy Committee may therefore wish to allow inflation to deviate from the target temporarily.

What about large shocks? The Remit continues:

In exceptional circumstances, shocks to the economy may be particularly large or the effects of shocks may persist over an extended period, or both. In such circumstances, the Monetary Policy Committee is likely to be faced with more significant trade-offs between the speed with which it aims to bring inflation back to the target and the consideration that should be placed on the variability of output.

In forming and communicating its judgements the Committee should promote understanding of the trade-offs inherent in setting monetary policy to meet a forward-looking inflation target while giving due consideration to output volatility. It should set out in its communication:

the outlook for inflation and, if relevant, the reasons why inflation has moved away from the target or is expected to move away from the target;

the policy action the Committee is taking in response;

the horizon over which the Committee judges it is appropriate to return inflation to the target;

the trade-off that has been made with regard to inflation and output variability in determining the scale and duration of any expected deviation of inflation from the target; and

how this approach meets the government’s monetary policy objectives.

In short, the MPC has considerable discretion to shape the public’s understanding of the inflation process and the trade offs involved when aiming for the 2% target.

Moreover, the MPC can set the timetable for bringing inflation back to target given large shocks. A longer horizon might be needed to bring inflation back to target in the case of large or a series of shocks. But there ought to be no doubt that the MPC is committed to this target even if it cannot be hit at all times.

Stopping for gas

Put another way, the BoE’s Remit is straight out of the New Keynesian canon as developed during the 1990s and perhaps reflected best in the Science of Monetary Policy paper of Clarida, Gali and Gerter. Seldom is there a clearer example of a useful cross-over from academic consensus to practical policy.

And this framework seems to form the basis of Taylor’s speech.

Taylor notes how the latest global energy shock—triggered by the conflict in the Middle East—has pushed the UK back into a difficult “stagflationary” environment, where inflation rises while growth weakens. For the MPC this trade-off creates the challenge that tightening policy to control inflation risks deepening the slowdown, while easing to support growth risks letting inflation persist. Central banks are operating in a more uncertain, less stable world than in the pre-2008 era.

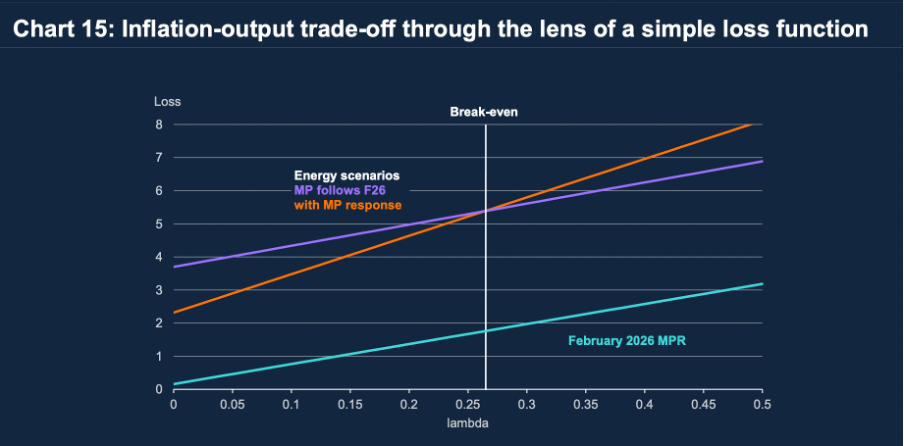

Taylor underlines the importance of λ (lambda) which is the weight policy makers place on the output gap in their loss function. λ = 0 means the policymaker only cares about the deviation of inflation from target, making them an “inflation nutter.” However, with λ > 0 the policymaker is concerned about the deviation of output from potential. The Bank’s Remit referenced above is implicitly endorsing that policymakers should be concerned about output as well as inflation.

And the higher λ the more inflation is allowed to deviate (temporarily) from target to cushion any hit to output.

Taylor then calculates the loss function for the MPC at this time given the supply shock, as shown in the chart below.

Compared to the February MPR inflation-output combination, the loss function due to the Middle East conflict is everywhere higher since inflation is expected to be higher. But should the policymaker respond? For the case where λ = 0 monetary policy should tighten (as on the far left of the chart) since the inflation nutter is willing to drive output far below potential to achieve a quicker return of inflation to target.

But higher λ implies a smaller policy response. And, curiously, Taylor find the point where the loss function with no new policy initiative compared to the February plans crosses a loss function with new tightening is where λ is slightly more than 0.25. And 0.25 happens to be the value of lambda that Bank staff believe is the historical weight on output stabilisation in past policy deliberations.

In other words, given typical concern for deviations of output from potential in the loss function, a BOE policymaker today should be roughly indifferent between sticking to the February policy plans and tightening policy further due to the recent shock.

Taylor cautions that while this thought experiment is enlightening, it may be too simple.

… in the real world, the economy may evolve differently.

If inflation came in worse, or concerns emerged about that risk via expectations un-anchoring, the policymaker might prefer the path of holding for longer (or, if bad enough, even hiking). In contrast, if those risks were low, and economic activity suddenly worsened, or signals suggested an elevated risk of such a downturn, the policymaker would want to be on the F26 path (or, if bad enough, cutting harder and faster, even below neutral). Put another way, either the circumstances or 𝜆 itself could change – or both. The only thing that is sure is that there are tough times ahead. We are heading into trade-off territory, the shock is non-negligible, and the task of calibrating policy is going to be difficult and potentially finely balanced.

Nevertheless, such reasoning presumably sits behind Taylor’s relatively more dovish paragraph in the recent monetary policy decision.

I think it appropriate to see us pausing to take stock, but inappropriate to infer a directional shift from this meeting… Given massive uncertainty around future energy prices, I currently see a high bar to hiking. I prefer to hold while we better gauge the shock. Policy can then be calibrated to deliver our 2% target, and we can take activist steps whenever needed.

In contrast, other MPC members were keen to point out they were “ready to act” which ought to go without saying—after all, if they were not “ready to act” at any of their policy meetings they would presumably be negligent. So the fact so many of the MPC wished to note that they are “ready to act” was a way of signalling they are open to hiking at the next meeting.

Communication breakdown?

Given the BOE Remit’s emphasis on the importance of forming and communicating its judgments in light of large shocks and difficult trade-offs, the March policy meeting’s ‘rushed’ communication looks like a potential failure by the MPC.

Indeed, it might be that the Bernanke Review has backfired.

The first test of the Bernanke Review was after the 2024 Autumn Statement, when the Bank more-or-less copied and pasted the OBR’s inflation projection into the Bank’s November MPR baseline. Since this inflation forecast turned out too optimistic, the Bank has since then been on the back-foot in terms of the inflation outturn and policy calibration.

We have now had a second test. The more recent decision to allow each MPC member a paragraph in the policy statement to express their view, which was not explicitly recommended by Bernanke, has introduced additional noise into the policy signalling.

Sometimes less is more.

In the Q&A after his speech, I asked Taylor about this process and whether there was “any attempt to moderate the overall tone so that the individual messages give a sort of a sense of the the median view on the committee.”

Taylor noted that

…the process of the individual paragraphs is is very individual… there’s a lot of stress on the fact that we are all individually accountable for our vote. So I think the paragraph is there specifically for us to explain, give our justification for our view of our outlook and why we’re voting the way we’re voting… [There is] an attempt to give you an aggregation and maybe there you know it’s more shaded and there’s an attempt to to reach sort of a consensus view or and at least in particular convey the view of the median voter who can change but you maybe doesn’t change that dramatically but it can change over time… so I think that’s that’s the way to to see the individual paragraphs as an addition uh that gives the individuals a way to to clearly communicate their own insight and perspective.

It is possible that the March meeting individual views were more hawkish than the aggregate message. If so, the attempt to improve communication has backfired.

As noted above, the Remit is clear that the MPC has a responsibility to communicate the need to deviate from target during large shocks. But the MPC instead rushed to communicate a willingness to hike despite the trade-offs.

Indeed, there are two main targets for Bank communication. The first is Main Street, and need to anchor inflation expectations to help improve future policy trade-offs. The second is the City, and the need to anchor the UK yield curve.

The MPC appears to have forgotten about the latter in an arguably panicked attempt to impact inflation expectations. And excessive focus on the former is a problem for the Treasury.

As such, on top of the wash-out of long UK rate positions from the initial supply shock, the MPC further exacerbated yield curve volatility by rushing out a policy message.

So much for the Remit with unfortunate repercussions for the fiscal outlook.

Conclusion: Will they do it?

Curiously, it remains to be seen what the MPC will actually do at the April policy meeting.

After all, what will the MPC know in April that they did not know in March?

They will know the March CPI and the length of the conflict, though the normalisation of energy markets is far from assured (and as seen in the US CPI figures, in March we will mostly have a headline impact from, the energy shock, while core effects will only be visible in later releases). And the MPC will have a set of scenarios by Bank staff which will cover a number of possible paths for inflation and unemployment (as part of the May MPR).

But which path are we in fact on? How can the MPC set policy based on staff forecasts given their recent reliance on inflation outcomes rather than forecasts to set policy?

My best guess is that it will be very hard to get consensus, after all, for a near-term BoE hike (given the challenges in the UK labor market).

In other words, despite signalling a willingness to act, the MPC might prefer to endorse Taylor’s viewpoint that it might still be better to hold to “better gauge the shock” than hike nearly-blind.

If you are interested in a full-summary of our 10-year anniversary conference in New York, please email anniversary@exantedatac.om

The content in this piece is partly based on proprietary analysis that Exante Data does for institutional clients as part of its full macro strategy and flow analytics services. The content offered here differs significantly from Exante Data’s full service and is less technical as it aims to provide a more medium-term policy relevant perspective. The opinions and analytics expressed in this piece are those of the author alone and may not be those of Exante Data Inc. or Exante Advisors LLC. The content of this piece and the opinions expressed herein are independent of any work Exante Data Inc. or Exante Advisors LLC does and communicates to its clients.

Exante Advisors, LLC & Exante Data, Inc. Disclaimer

Exante Data delivers proprietary data and innovative analytics to investors globally. The vision of exante data is to improve markets strategy via new technologies. We provide reasoned answers to the most difficult markets questions, before the consensus.

This communication is provided for your informational purposes only. In making any investment decision, you must rely on your own examination of the securities and the terms of the offering. The contents of this communication does not constitute legal, tax, investment or other advice, or a recommendation to purchase or sell any particular security. Exante Advisors, LLC, Exante Data, Inc. and their affiliates (together, “Exante”) do not warrant that information provided herein is correct, accurate, timely, error-free, or otherwise reliable. EXANTE HEREBY DISCLAIMS ANY WARRANTIES, EXPRESS OR IMPLIED.

Exante Data is a trading name of Vanda Research Limited which is an appointed representative of Messels Limited which is authorised and regulated by the Financial Conduct Authority.

Thanks, this is useful and illuminating. It is generally clear to a non- technical generalist, despite the complexities involved with the equations and quadratic function mathamatical jargon, partially explained in clear English.

Also the speech by Taylor was also clear, relevant and helpful and worth reading by non-insiders.

A couple of naive questions/requests.

The seventies while a decade of rampant inflation and steadily rising unemployment was also one of real per capita national and household income growth. Was it that bad from an economic rather than political stability angle?

It would be helpful for the 'new keynesian canon' to be crisply explained in a paragraph or two, extending beyond that it models downward sticky nominal wages.