Correlation and macro analysis

Why (and when) might correlation analysis mislead (or be helpful)?

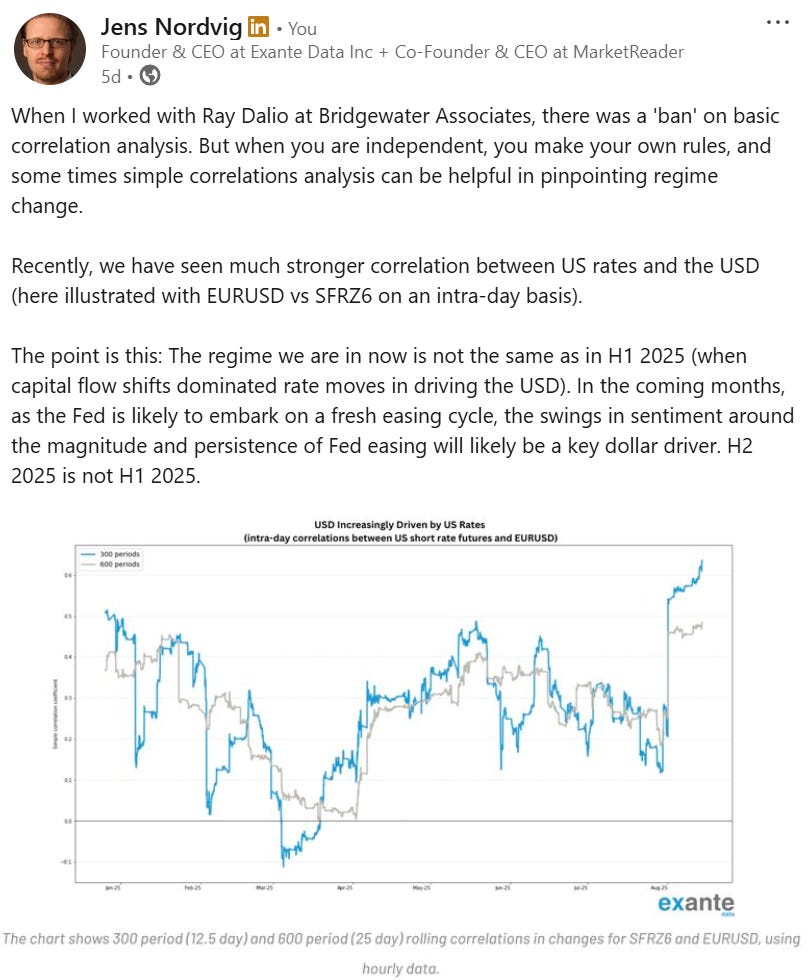

Earlier this week, I wrote a quick LinkedIn post about correlation analysis, with reference to Ray Dalio's “ban” on such analysis when at Bridgewater Associates during the Global Financial Crisis. This post, which went semi-viral, is posted below:

I have since been asked many questions about this “ban” and what was behind it. Hence, the longer version of the story is this.

What not to do?

In 2008, I was a Managing Director at Goldman Sachs, in charge of currency analysis. And when I joined Bridgewater Associates in early 2009, I learned (to my surprise) that use of correlation analysis was frowned upon, and generally discouraged.

Specifically, Bridgewater had an internal course for new analysts that used Goldman Sachs research (a tool to track correlations dynamically) as the type of research not to do.

The arguments were the familiar ones (my interpretation):

Correlations are inherently unstable;

They change as the interaction between structural forces in the economy evolve (and time is better spent understanding the underlying forces);

Spending too much time on correlations also means that focus drifts away from understanding underlying drivers, and more towards “market sentiment” (which can be wrong and typically a waste of time for medium-term investing);

Hence, paying too much attention to market correlations may risk a bias towards “trend following” (as opposed to true contrarian independent thinking.)

But Ray Dalio is not the first macro investor to lament the usefulness of correlation analysis.

Keynes and Soros

We should recall Keynes’ concern (in Collected Works XIV) with Tinbergen’s early econometric work on business cycles in the early-1940s: market behaviour might not respond to external events in the same way every time; the econometrician could miss important drivers of macro-outcomes; moreover, coefficients might not be constant through time:

The coefficients arrived at are apparently assumed to be constant for ten years or for a longer period. Yet, surely we know they are not constant. There is no reason at all why they should not be different every year.

When expressing such concerns, we might suppose that Keynes was wearing his, by this point rather experienced, macro-investor hat.

The same insight can also arguably be derived from George Soros’ famous concept of reflexivity: market participants try and understand the world, but also participate in the world. This creates a two-way interaction between understanding and participating which makes simple market relations unlikely to persist as the two feed on each other. In such a world, formal mathematical and econometric modelling is doomed to failure as discussed by Tony Lawson.

Once more, an experienced macro-investor understands that the world cannot be boiled down to simple correlations.

Back to correlation

Put another way, economics is a tricky profession indeed.

We are capturing macro-variables and market prices based on human and governmental behavior; the market correlations that derive from that are far from stable.

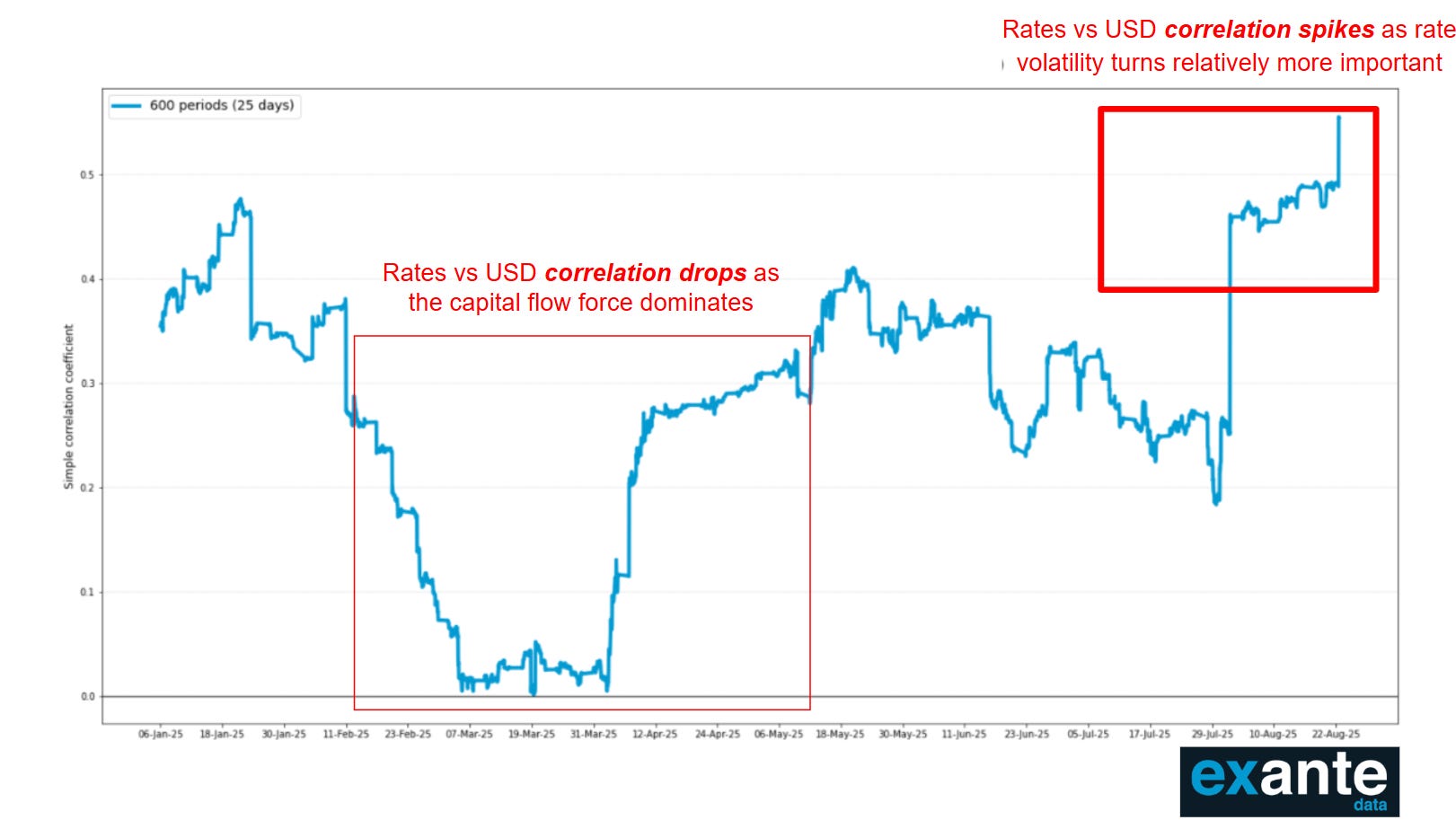

As as result, correlations that are steady above, say, 30%, as with US rates and EURUSD in the chart above, might be considered “high”—whereas this would be viewed as poor in many other settings.

A summary of technical critiques of correlation analysis note problems such as:

Correlation does not imply causation—a classic;

Instability—whereby, correlations will change through time, as Keynes noted;

Volatility effects—which can bias correlation effects;

Non-linear relationships;

Omitted variables—where a third variable drives the correlation between two assets that should be controlled for;

One special case of the first point is spurious correlation between trending variables (I am from Denmark - ‘the land of co-integration’; hence this is a topic that was a big part of econometrics 1, 2, 3, etc when I studied at University of Aarhus quite a few years ago).

Take a recent example we have been focussing on this year.

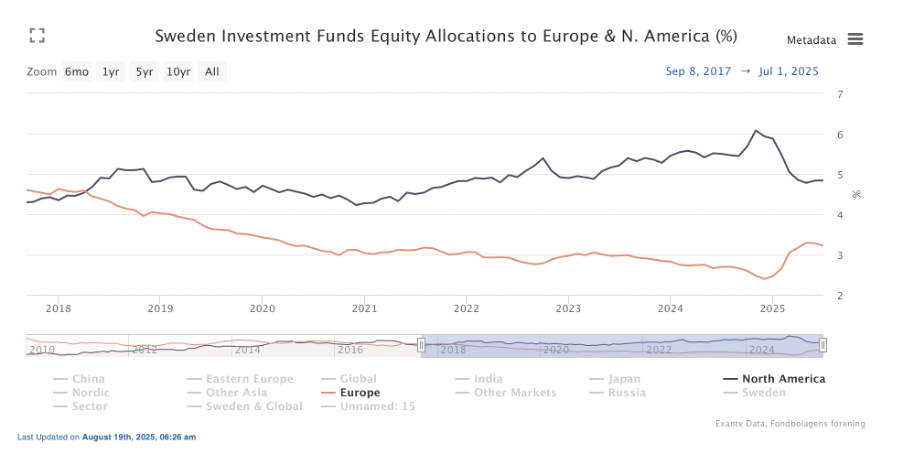

Per a recent previous post, capital flows into the United States were interrupted in the first half of this year after a long period of US outperformance and exceptionalism.

For example, the equity allocation of Swedish investment funds between North America and Europe is shown below—allocations shifted away from the former towards the latter around the turn of this year, though has levelled off again in the past two months.

Perhaps unsurprisingly, such a shift in global investor sentiment towards the United States weighed on the dollar, disrupting the “usual” correlation between rates and the dollar.

But this is the point!

A mosaic approach as suggested in our tracking of US capital flows would suggest the typical rates correlation would dip below normal in H1 2025. And our analysis now points to less force from this source in H2 (as discussed in public here). Hence it is logical that the correlation would move back higher (normalize) once more, when this third variable moves in the background.

Hence we are now focussed on the US rates narrative as a driver of the dollar once more—that is, until events interrupt the story once more.

Conclusion

Important macro-investors have over history lamented excessive reliance on simple time series relations when coefficients can change or when the discipline of understanding deeper structural drivers of asset prices is called for.

But simple correlations (or more sophisticated multidimensional models such as SVARs) can provide insights into the drivers of asset prices still. Hence we use them as part of a broader market narrative to inform strategy; as an objective way of cross-checking which regime we are currently in (without assuming that those correlations will stay constant).

Perhaps the secret is to be nimble—and never be wedded to historical relations when structural forces or capital flows can quickly interrupt past correlations. In fact, the best market opportunities are typically those that involve and anticipated regime change; a change that the market is not yet pricing in spot or volatility instruments

In the second half of 2025, our core view has been that the USD would re-couple with US rates, as the force from capital flows was waning and rate volatility more important. And this is indeed playing out. It is suitable to end this piece with an updated correlation chart (including Friday’s price action around Jackson Hole) that illustrates this…

Thanks to Chris Marsh for input in relation to historical critiques of correlation analysis.

The content in this piece is partly based on proprietary analysis that Exante Data does for institutional clients as part of its full macro strategy and flow analytics services. The content offered here differs significantly from Exante Data’s full service and is less technical as it aims to provide a more medium-term policy relevant perspective. The opinions and analytics expressed in this piece are those of the author alone and may not be those of Exante Data Inc. or Exante Advisors LLC. The content of this piece and the opinions expressed herein are independent of any work Exante Data Inc. or Exante Advisors LLC does and communicates to its clients.

Exante Advisors, LLC & Exante Data, Inc. Disclaimer

Exante Data delivers proprietary data and innovative analytics to investors globally. The vision of exante data is to improve markets strategy via new technologies. We provide reasoned answers to the most difficult markets questions, before the consensus.

This communication is provided for your informational purposes only. In making any investment decision, you must rely on your own examination of the securities and the terms of the offering. The contents of this communication does not constitute legal, tax, investment or other advice, or a recommendation to purchase or sell any particular security. Exante Advisors, LLC, Exante Data, Inc. and their affiliates (together, "Exante") do not warrant that information provided herein is correct, accurate, timely, error-free, or otherwise reliable. EXANTE HEREBY DISCLAIMS ANY WARRANTIES, EXPRESS OR IMPLIED.

Really enjoyed this, Jens.

I think you frame the core issue well. The problem isn’t correlation analysis per se, it’s the assumption of coefficient stability. In a system driven by capital flows, funding conditions, and shifting policy narratives, relationships are necessarily regime-dependent.

The USD vs rates example this year is a good illustration. In H1, capital flow rotation appeared to dominate rate differentials. As that force wanes and rate volatility becomes relatively more important, that particular correlation reasserts itself. That doesn’t make either regime more “true” than the other, it just reflects which variable is marginal at the time.

To me, correlations are best treated as diagnostic tools. When they strengthen or weaken, that change itself is information about what force is currently in control. The instability is the signal.

Appreciate you walking through the longer backstory here.

This is a great one, Jens. Thanks for sharing!