Milei's magic?

BCRA balance sheet clean up in 2024

ARGENTINA has been in the news over the past year for the remarkable fiscal adjustment initiated since the change of government and, more recently, the sharp slowdown in inflation and return to growth—suggestive that Milei’s plan is bearing fruit.

Less commented, however, has been progress in cleaning up the central bank balance sheet (BCRA.)

Balance sheet blues

As noted previously, any chance of macroeconomic stabilisation in Argentina in recent years has been undermined by the fact that the BCRA was issuing near-money liabilities at a very high interest rate—but had no interest bearing assets to absorb the cost of these liabilities. This was a quasi-fiscal deficit that continually undermined stabilisation efforts as it meant that BCRA in the end had to monetise the cost of policy—which in turn meant a weaker currency and, given liability dollarisation, higher debt-to-GDP.

Despite the illusion of tight money, BCRA was in fact running an ever-expanding balance sheet resulting in ARS depreciation and inflation.

Clean up

Over the past 12 months, however, especially from the middle of the year, there has been a substantial balance sheet clean up.

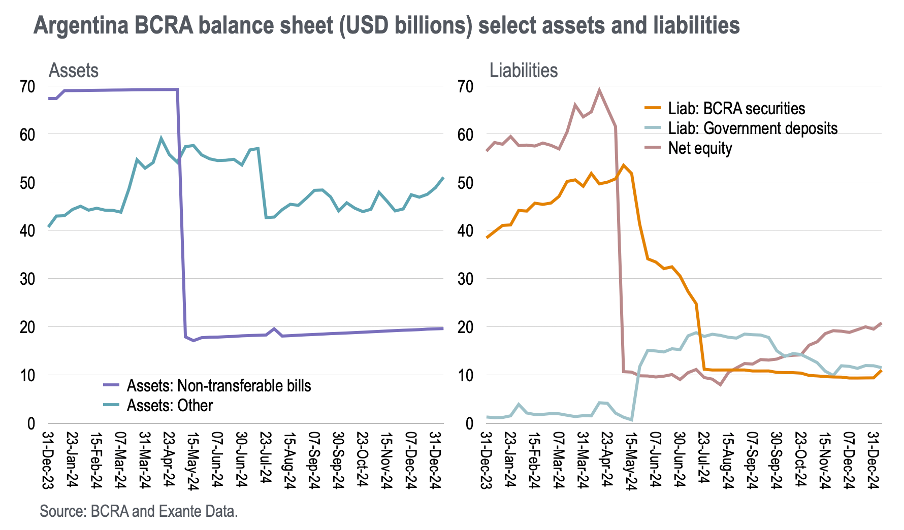

BCRA held about USD70bn in “non-transferable bills” heading into 2024. These were reduced in size by about USD50bn from late April. Initially this was achieved simply by writing down net equity on the liabilities side—while interest bearing securities remained elevated at about USD50bn.

From late-May these BCRA securities were also reduced substantially—from about USD50bn to about USD10bn by mid-July.

In other words, the non-interest bearing dollar assets have been reduced by about USD50bn while interest bearing local currency liabilities have been reduced by about USD40bn.

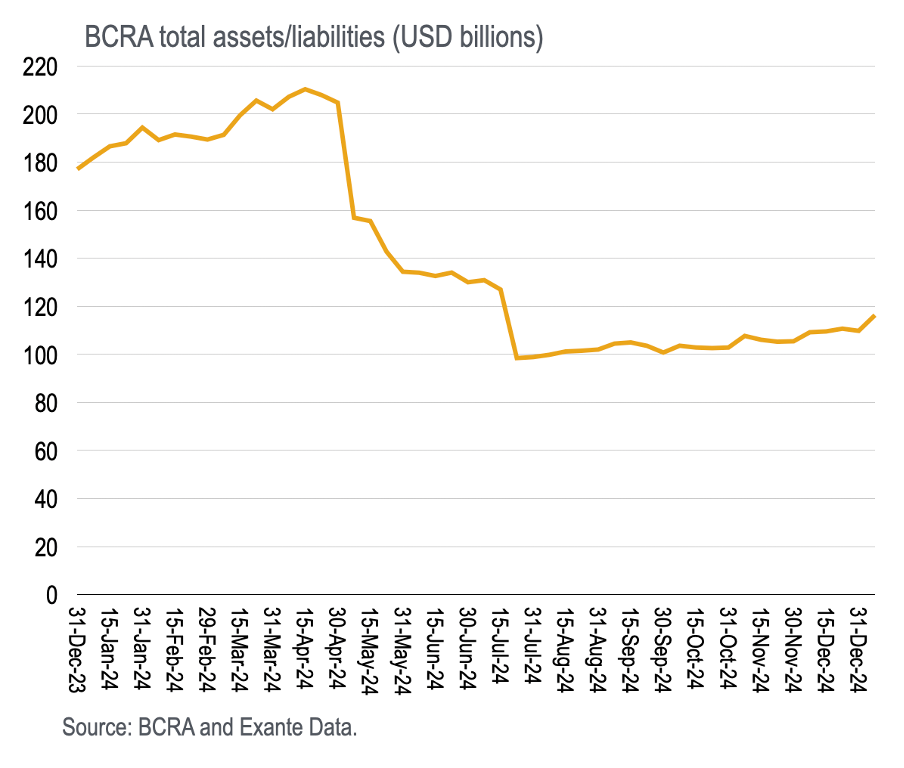

Seen in terms of the total assets of the central bank, BCRA balance sheet has contracted about USD100bn between April and June, roughly halving in size.

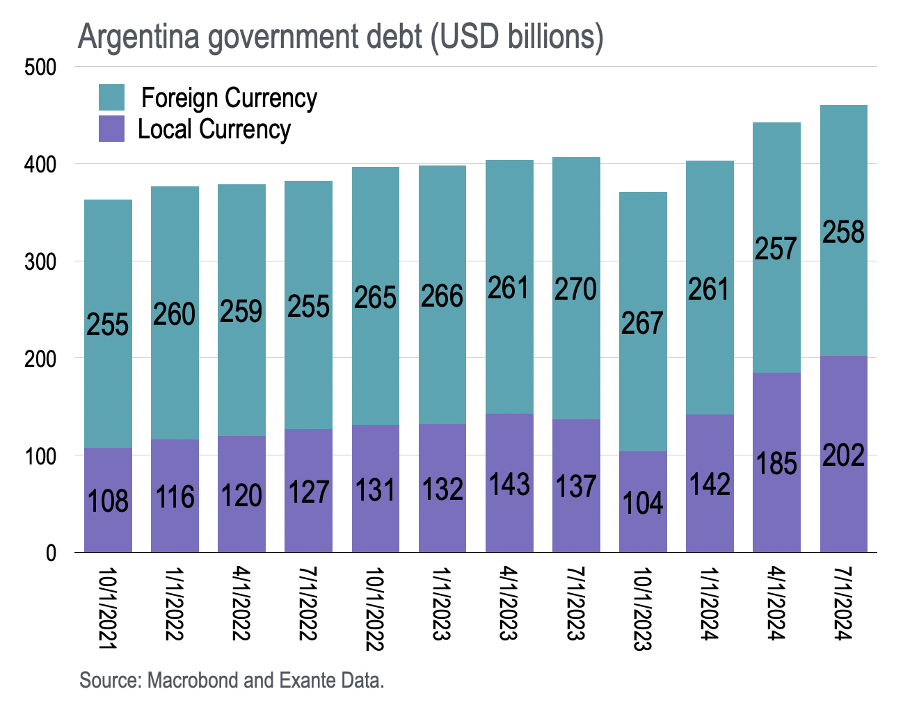

How was this achieved? There has been no plan written down, to my knowledge, but the dollar value of government debt has increased from USD370bn as of end-2023 to USD460bn as of end-2024Q3 mostly due to the expansion of local current debt—which has increased about USD100bn. So despite the primary fiscal surplus and modest interest on government debt, outstanding government liabilities has increased sharply.

A crucial step forward

This adjustment means the local currency debt on the BCRA balance sheet has migrated to the government—as it should.

Ideally, this lengthens the average maturity of consolidated government liabilities and formally transfers the interest burden onto the fiscal authorities—so the central bank will not be forced to monetise future interest costs but these will instead to met through a primary fiscal surplus.

As well as the fiscal adjustment, this balance sheet clean-up is a crucial step forward for Argentina—something that has been delayed for at least 6 years under the IMF program.

Indeed, the IMF published a(nother) Ex-Post Evaluation of the latest program last week, and on page 32 they note how under the program, deadlines for a balance sheet clean-up came and went, and were eventually dropped:

At last, the clean-up has begun.

It is remarkable that, despite all the eggheads and boffins at the IMF overseeing the Argentina program for the past 6 years, they were unable to assemble a consistent macro-financial program—instead it has taken a chainsaw-wielding maniac President to do their dirty work.

While this is indeed good news, a glance at the external accounts suggest there are problems still—something we will address shortly.

The content in this piece is partly based on proprietary analysis that Exante Data does for institutional clients as part of its full macro strategy and flow analytics services. The content offered here differs significantly from Exante Data’s full service and is less technical as it aims to provide a more medium-term policy relevant perspective. The opinions and analytics expressed in this piece are those of the author alone and may not be those of Exante Data Inc. or Exante Advisors LLC. The content of this piece and the opinions expressed herein are independent of any work Exante Data Inc. or Exante Advisors LLC does and communicates to its clients.

Exante Advisors, LLC & Exante Data, Inc. Disclaimer

Exante Data delivers proprietary data and innovative analytics to investors globally. The vision of exante data is to improve markets strategy via new technologies. We provide reasoned answers to the most difficult markets questions, before the consensus.

This communication is provided for your informational purposes only. In making any investment decision, you must rely on your own examination of the securities and the terms of the offering. The contents of this communication does not constitute legal, tax, investment or other advice, or a recommendation to purchase or sell any particular security. Exante Advisors, LLC, Exante Data, Inc. and their affiliates (together, "Exante") do not warrant that information provided herein is correct, accurate, timely, error-free, or otherwise reliable. EXANTE HEREBY DISCLAIMS ANY WARRANTIES, EXPRESS OR IMPLIED.