Tariffs and commodities: smoke but no fire

Tariffs have a highly predictable impact on the pricing of homogeneous goods, like refined metals. Markets are yet to reflect this.

Commodity markets are efficient with respect to how they clear. They are woefully inefficient in terms of their ability to discount future information beyond the liquidity bulge at the very front-end of the curve. The last year or so has highlighted this imperfection. The silence of the metal forwards, despite the near certainty that tariffs were coming, illustrates this perfectly.

When a tariff is imposed on a homogeneous commodity, and the marginal unit in the importing country comes from abroad, theory and logic suggest that the price level behind the tariff wall will converge on the delivered cost of the product, plus the tariff imposed. The delivered cost equals the home price in the exporting region, plus freight to the buyer (i.e. “CFR” terms).

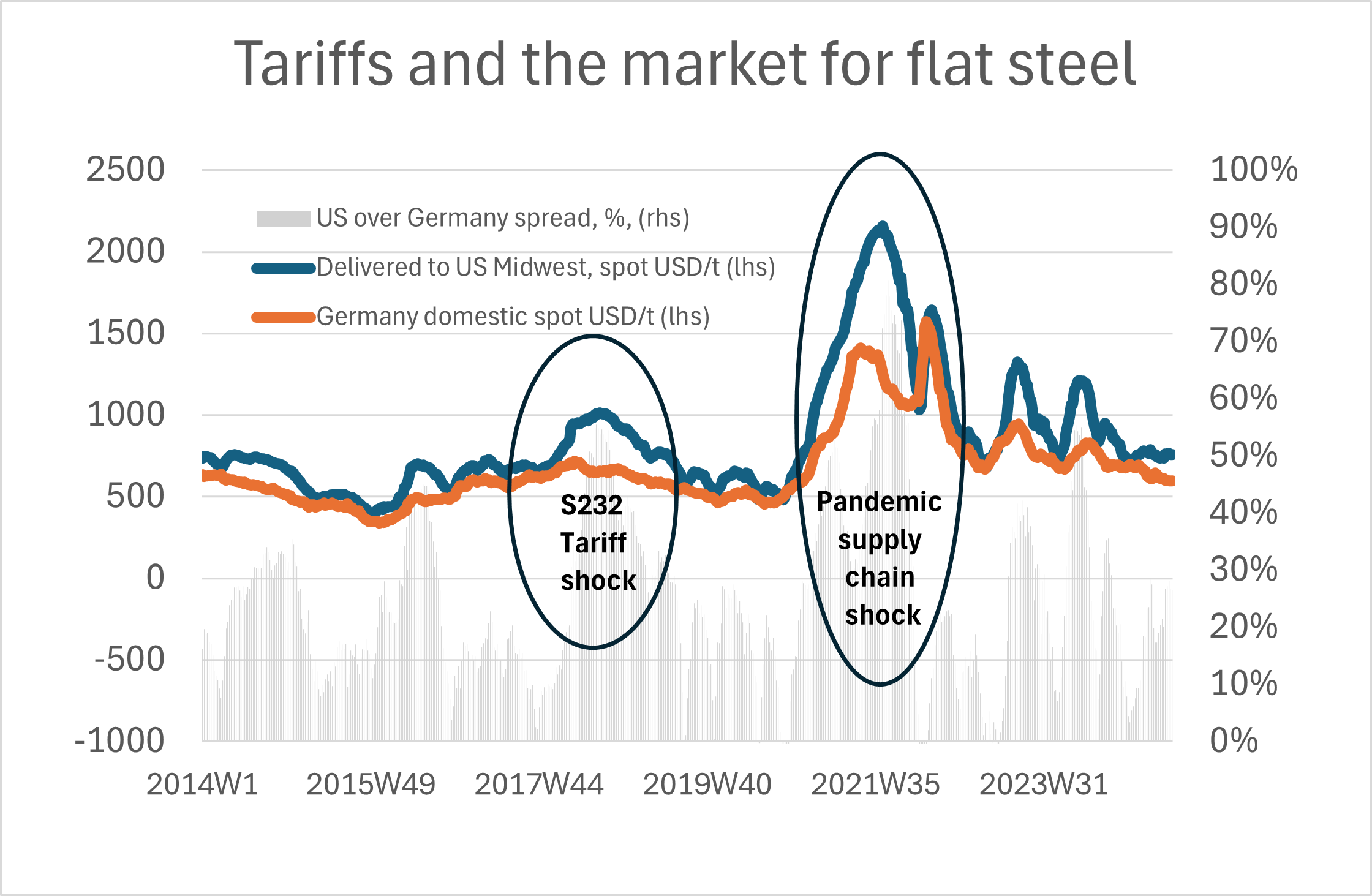

This logic played out in the real world when 25% tariffs were imposed on steel imports under the “S232” national security loophole back in 2018. US hot rolled coil (HRC) steel prices gapped higher and the spread to the rest of the world has been maintained since. The chart below shows German prices. The spread to China is even more pronounced.

Figure 1: regional steel markets since the S232 tariffs of 2018

The most efficient method for forecasting US prices became to run a simple regression on HRC CFR by your choice of region to the US and then append the tariff rate. The result has been a comfortable domestic operating environment for the US’ highly concentrated home industry, and wildly uncompetitive steel input costs for industries sitting downstream. The latest data show that flat steel is 29% more expensive at the factory gate in the US than in Western Europe and approximately double the equivalent price in China. Double.1

Fast forward to today, and universal tariffs are pending. Commodity markets are braced for the potential fallout on the demand side (copper gapped lower on the election result back in November, and prices fell again as day one executive orders hit the newswires), but there seems to have been very little market activity looking to take speculative advantage of (or hedge against on the physical side) the imminent distortions that are likely to play through in base metals.

If commodity markets were more efficient and forward looking, with more evenly disbursed liquidity pre-and-post 3 months, a tariff-sized step change in 2025 contracts for copper, zinc and lead (three exchange traded commodities where the US is an importer of refined metal: note aluminium was swept up in the 2018 S232, albeit with exemptions carved out, so it is not a clean read like the other three) should have been partially priced into US exchange contracts throughout the 2024 campaign, driving a distinct premium over LME pricing.

(The AI-euphoria and low US stocks that drove COMEX copper prices to all-time highs, with massive LME arbs, in the first half of 2024 was an independent event).

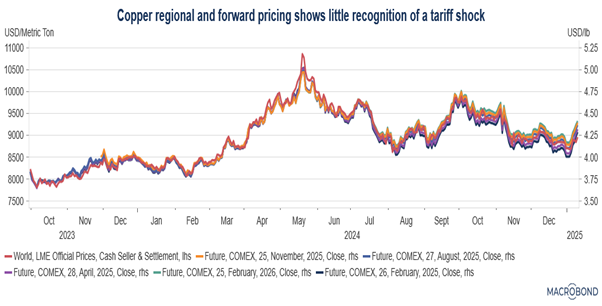

Once the election result became known, arguably the pricing of 2025 contracts should have been speculating on three things: the timing and size of any tariff, and if the tariffs were not uniform, how that would impact upon the marginal unit of metal supply to the US: in much the same way as fixed income markets speculate on both the scale of overall policy rate movements and at which meetings the changes will occur. Metals markets? There was precisely nothing discernibly priced in until the spread between COMEX and LME prompt copper pricing began to move a little higher in recent weeks.

Figure 2: LME settlement price and COMEX copper contract schedule (Feb/Apr/Aug/Nov 2025, Feb 2026) since the start of 2024: US futures hug the global base price.

And even then, market commentary centered for a few days on the mystery of the gap, and the new administration’s day one executive orders once again pushed prices lower on demand concerns, despite an apparently modest opening gambit with respect to Chinese tariffs.

If there was anything priced in, it is reasonable to suggest that prices should have gone higher to recalibrate to a potentially smaller shock. In tandem with the election day price drop, this sort of price action might be dubbed “sell the rumour, sell the fact”.

These tariff driven arbitrage opportunities are still, broadly, hiding in plain sight. Additionally, metal that is already sitting in the US will be the passive beneficiary of the tariff price gap, without having actually absorbed the tariff cost to enter the country. That is a veritable free lunch for producers and owners of physical metal in the value chain – all else equal.

The massive gap in steel prices between the US and China is a practical argument for security analysts to use PPP measures of GDP when making international comparisons, which adjust for different price levels across countries. Using current dollar GDP as a proxy for economic heft is equivalent to arguing that a tonne of steel in the US is twice as useful as the same tonne in China. I will develop this point in more detail at a later date.

The content in this piece is partly based on proprietary analysis that Exante Data does for institutional clients as part of its full macro strategy and flow analytics services. The content offered here differs significantly from Exante Data’s full service and is less technical as it aims to provide a more medium-term policy relevant perspective. The opinions and analytics expressed in this piece are those of the author alone and may not be those of Exante Data Inc. or Exante Advisors LLC. The content of this piece and the opinions expressed herein are independent of any work Exante Data Inc. or Exante Advisors LLC does and communicates to its clients.

Exante Advisors, LLC & Exante Data, Inc. Disclaimer

Exante Data delivers proprietary data and innovative analytics to investors globally. The vision of exante data is to improve markets strategy via new technologies. We provide reasoned answers to the most difficult markets questions, before the consensus.

This communication is provided for your informational purposes only. In making any investment decision, you must rely on your own examination of the securities and the terms of the offering. The contents of this communication does not constitute legal, tax, investment or other advice, or a recommendation to purchase or sell any particular security. Exante Advisors, LLC, Exante Data, Inc. and their affiliates (together, "Exante") do not warrant that information provided herein is correct, accurate, timely, error-free, or otherwise reliable. EXANTE HEREBY DISCLAIMS ANY WARRANTIES, EXPRESS OR IMPLIED.